Index

CATEGORY

The Pros and Cons of Automating Underwriting Processes at Banks

Automating underwriting equips credit teams with the scale, trust, and efficiency to grow loan origination. Key considerations to make before automating undewriting include controls around data qualify, verification systems, and complexity of integration.

Nov 28, 2024

In the era of digital transformation, banks are leveraging automation to optimize operations and enhance customer experiences. One area where automation has made significant strides is underwriting—the process of assessing the creditworthiness of borrowers.

While automating underwriting processes brings a range of benefits, it must be navigated carefully with a focus on first principles of data collection. This blog explores the benefits of automated underwriting flow and considerations to make before automating underwriting processes at banks or credit unions.

Pros of Automating Underwriting Processes

1. Increased Efficiency

Automation streamlines the underwriting process by reducing manual tasks such as data entry, document verification, and risk analysis. This leads to faster loan processing times and allows banks to handle higher volumes without compromising accuracy.

2. Consistency and Accuracy

Automated systems eliminate human errors and ensure consistent application of underwriting criteria. By relying on predefined algorithms and data models, banks can reduce biases and make decisions based on objective metrics.

3. Cost Savings

Automating underwriting can reduce operational costs by minimizing the need for extensive manual labor and improving resource allocation. Banks can reinvest these savings into other strategic initiatives.

4. Improved Customer Experience

Faster processing times and more accurate decisions enhance the borrower’s experience. Automation enables banks to provide real-time updates and quicker approvals, increasing customer satisfaction and loyalty.

5. Scalability

Automated underwriting systems are scalable and can handle growing volumes of applications as banks expand their operations. This scalability is crucial for accommodating peaks in demand without sacrificing performance.

6. Better Risk Management

Advanced algorithms and predictive analytics enable more sophisticated risk assessment. Automated systems can analyze vast amounts of data, identify patterns, and flag potential risks that might be overlooked in manual processes.

Considerations When Automating Underwriting Processes

1. Initial Implementation Costs

Implementing an automated underwriting system may require significant upfront investment in technology, software, and training. For smaller banks, the tax on resources has been prohibitive.

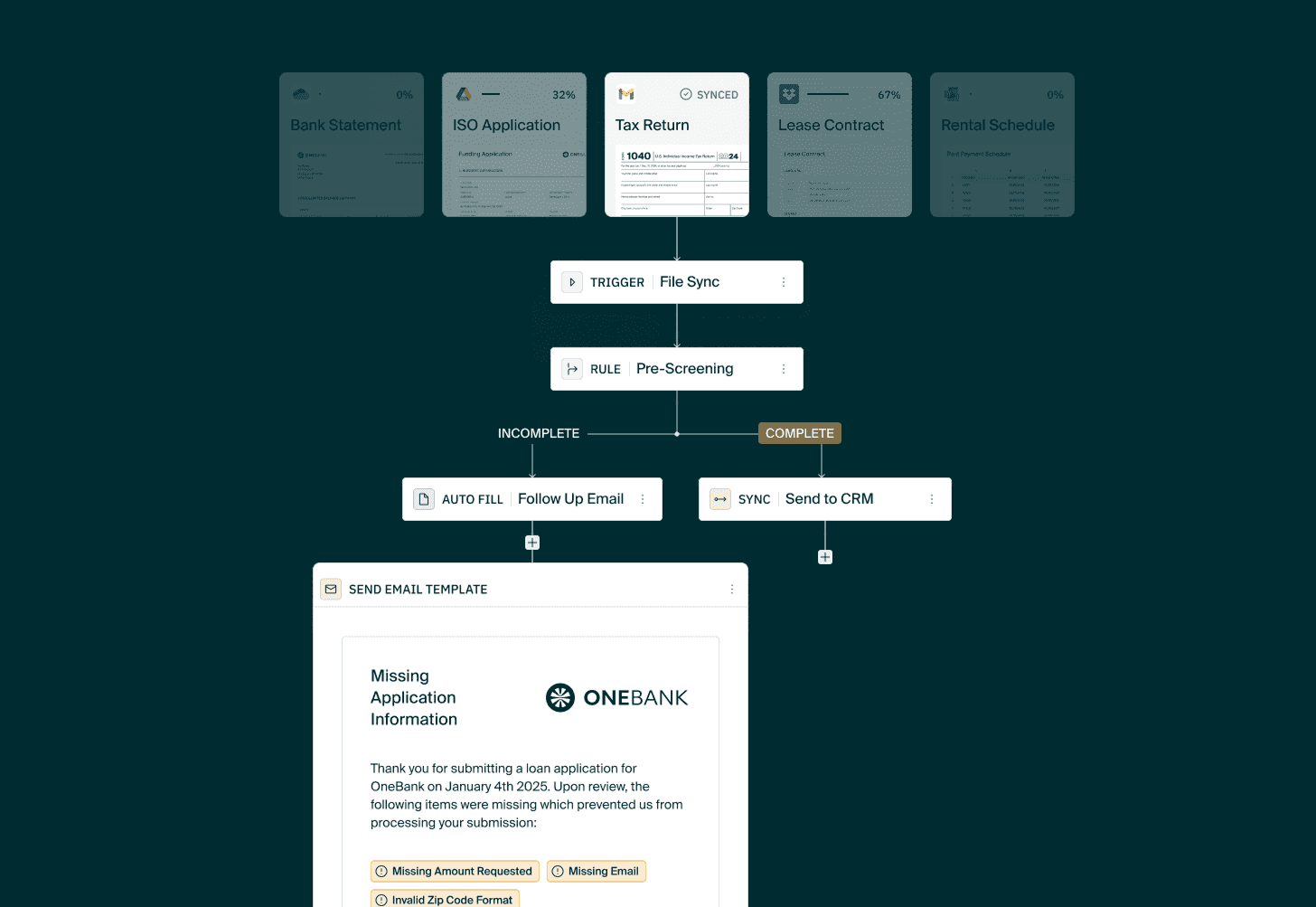

SOLO is a platform that grants high functionality to teams without the need for expensive ongoing technical support. Our low-code platform is fully customizable, and can fully integrate in existing workflows.

2. Complexity of Integration

Integrating automated systems with existing infrastructure and workflows can be complex and time-consuming. Ensuring compatibility with legacy systems and maintaining data consistency requires careful planning.

SOLO's implementation team works hand in hand with lenders for a successful rollout of the 01 PULL platform. Even the most complex underwriting process can be fully replicated as easy to use, simple to customize workflows.

3. Dependence on Data Quality

The reliability of automated underwriting systems depends heavily on the quality of data inputs used for the system. Incomplete, outdated, or inaccurate data can lead to flawed decisions and increase the risk of defaults.

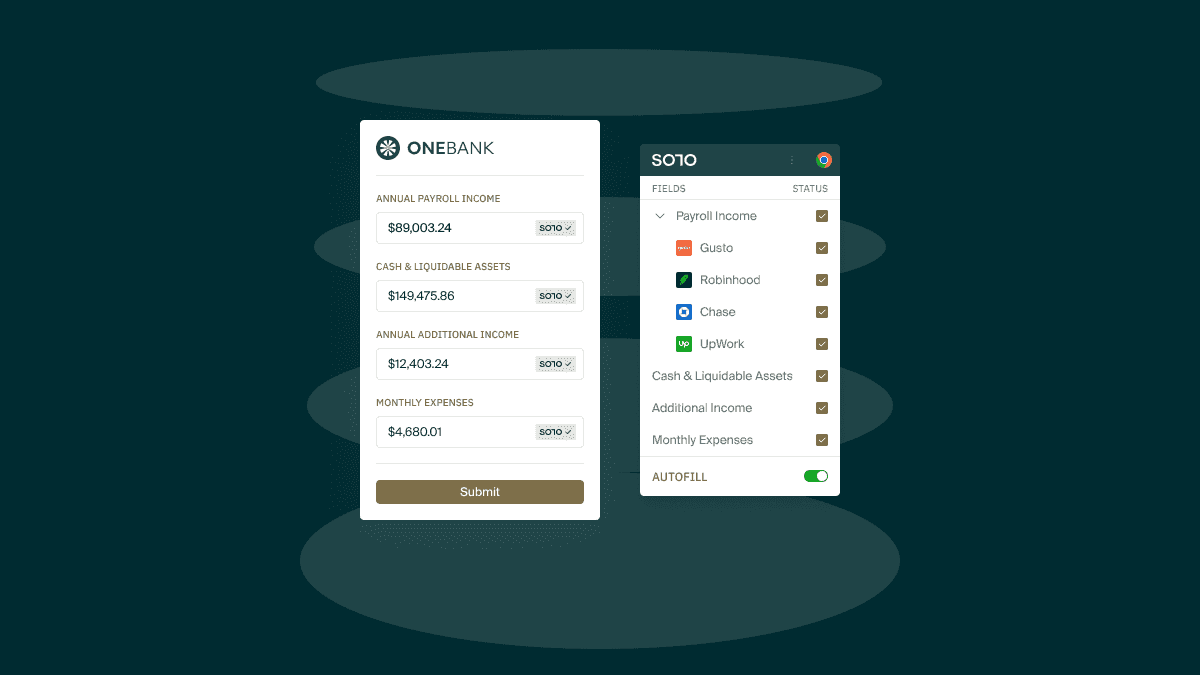

SOLO shifts the focus within the automated underwriting workflow from just a decision, to also encompass best practices of data collection and activation. A shift from self reported financials to autonomously constructed financials within our automated underwriting platform enhances the integrity of a decision engine. Learn more about how it works.

4. Choose a System that Does Not Limit Flexibility

Automated systems follow predefined algorithms and may struggle to accommodate unique or unconventional cases. This lack of flexibility could lead to the rejection of viable applicants who do not fit standard criteria.

SOLO brings highly advanced functionality with a low code interface, so technical and nontechnical teams alike are empowered with the ability to customize their underwriting automation.

5. Protect Against Fraud Risks

With increased reliance on digital systems comes heightened exposure to fraud if the appropriate data governance is not in place.

SOLO creates a radically transparent system for credit, where every data point is traceable, auditable, and verified. When choosing a solution for automated underwriting, ensure the system accounts for transparency at every step.

6. Avoid Algorithmic Bias

Although automation aims to reduce bias, poorly designed algorithms or training data can inadvertently introduce or perpetuate discriminatory practices. Continuous monitoring and adjustments are essential to ensure fairness.

7. Maintain Regulatory Compliance

Automated underwriting systems must comply with stringent regulations. Keeping up with evolving compliance requirements and ensuring transparency in decision-making can be challenging if using a system that neglects current and evolving laws.

SOLO is proud to advocate for policy that fosters innovation and trust in the modern credit ecosystem. Listen to our founder speak on CFPB's 1033 Final Rule in this year's American Fintech Policy Summit.

Safely Roll Out Automated Underwriting

While automation offers significant advantages, banks must approach it strategically to maximize benefits and mitigate risks. Here are some best practices for achieving this balance:

Start Small: Pilot automation in specific underwriting segments before scaling across the organization.

Focus on Data Quality: Invest in robust data management practices to ensure accuracy and reliability.

Begin with Human Oversight: Combine automation with human expertise to incrementally develop internal policies and adoption of an automated underwriting system.

Regularly Audit Algorithms: Continuously monitor and update algorithms to minimize bias and adapt to changing market conditions.

Prioritize Borrower Experience: Safeguard sensitive information and build customer trust by providing users with a frictionless, secure, and user friendly interface to leverage their credit data.

Automating underwriting processes has the potential to revolutionize banking operations, offering efficiency, accuracy, and enhanced customer experiences. However, the transition to automation must be managed thoughtfully to address challenges such as data quality, cybersecurity risks, and regulatory compliance. By a thoughtful approach to data collection for automated underwriting process, banks can leverage new technology to stay competitive in an increasingly digital landscape while reducing risk.