Index

CATEGORY

Best Practices

Automation for Relationship Banking: Using AI to Put People First

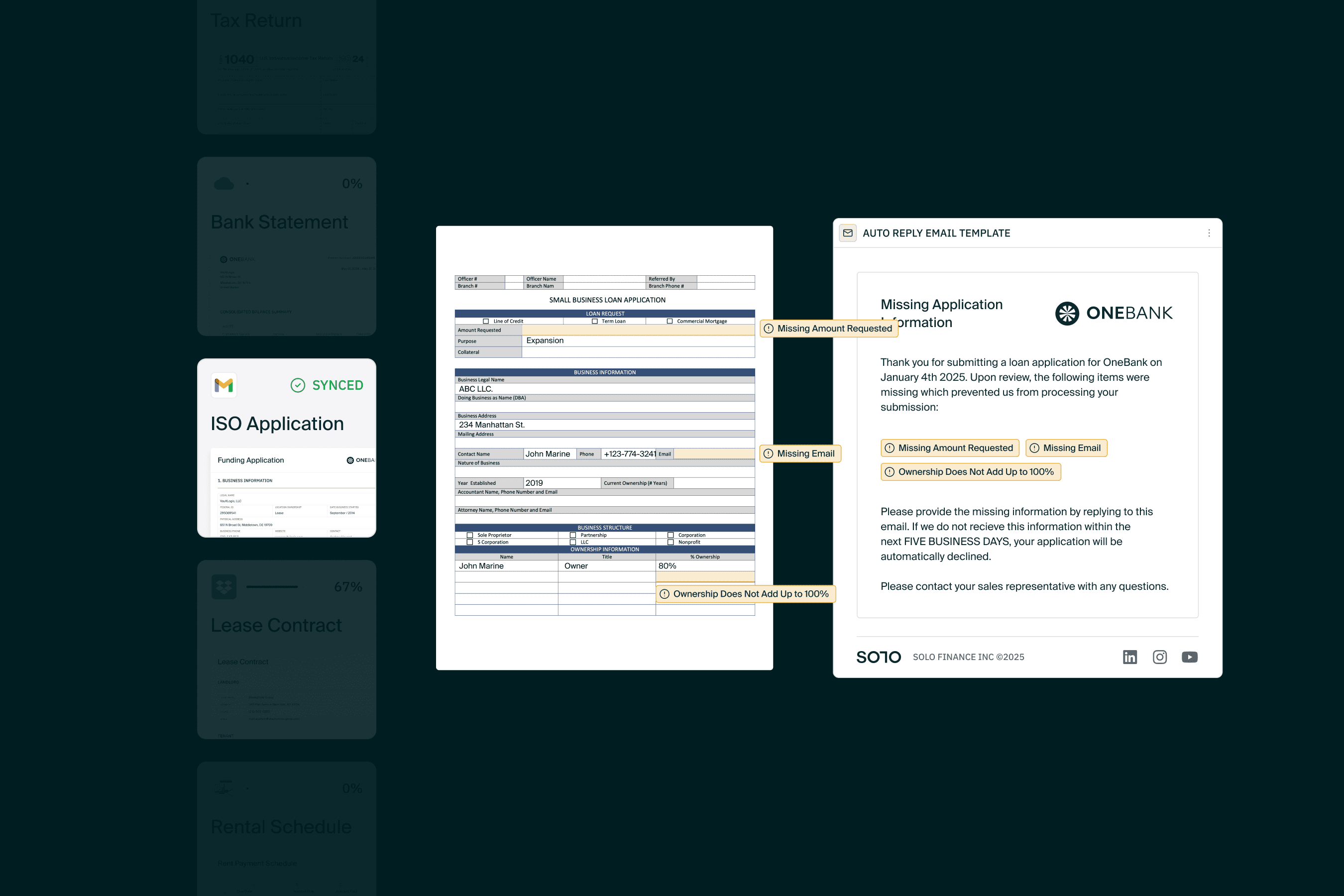

Credit Underwriting Automation can and should be leveraged not just for process efficiency, but to grow and strengthen banker-small business relationships.

Feb 6, 2025

There’s a conversation we keep having with bankers this year. How do we build digital products that rival a fintech in scale and speed, without compromising on risk tolerance, accuracy, and customer relationships

It’s not surprising that this is on the forefront of many bankers’ minds. Just look back at what’s happened the last few years:

In 2021 fintechs burst on the scene to dominate quick lending, taking opportunities (and deposits) from banks.

2023 saw the pendulum swing back as some fintechs crashed publicly, tipping the scales of customer favor back to banks.

2024 was the year banks tried to compete with fintechs on speed—and let’s be honest, that’s a race they’re unlikely to win (and maybe shouldn’t even try).

Now banks, and particularly community banks, find themselves at what feels like an impossible crossroads.

In reality they’re the ones with the competitive advantage, even in the AI age.

The best opportunity banks have to regain market share (and come back to their identity) is to focus on what they do best: building relationships and fostering collaboration, but using automation to scale that.

This is going to require a fundamentally different approach to the current application of AI and automation (or lack thereof) in lending processes.

In the past, automation has made decisions faster and more efficient, but it’s come at a cost: the agency of both the banker and the customer.

A quick “yes” or “no” may save time, but it doesn’t help customers understand how to qualify for what they want. Nor does it allow bankers to guide their customers toward better financial outcomes. Real opportunity is left on the table while customers are rushed out the door unless they fit a rigid algorithm.

Banks don’t need to win the speed race. They can (and should) be faster, but they don’t have to be the fastest players to win. Instead, it’s time we fix process inefficiencies so that we can then focus on the bigger picture.

How do we turn a single chance to underwrite, approve, and fund into a continuous partnership?

Can we make it so that a customer only has to introduce themself once for us to always know what they need, and how to get them to future goals?

How do we innovate our product mix to meet the customers demands and needs while sustainably preparing for the future?

Banks can—and should—lean into the power of relationships and personalized advice made scalable with automation. That’s where trust is built, and real value is created.

Relationships made scalable will be key to winning back market share in the end.