Index

CATEGORY

Best Practices

The Loan Origination Process

Nov 8, 2024

The loan origination process refers to the entire series of steps involved in creating, evaluating, approving, and disbursing a loan to a borrower. It encompasses everything from the initial loan inquiry to the disbursement of funds and includes tasks such as application, verification, risk assessment, and approval.

The loan origination process can be manual, automated, or a hybrid of both, depending on the institution’s capabilities. Automation tools, such as Loan Origination Systems (LOS), help streamline this process, improve accuracy, and enhance the borrower experience.

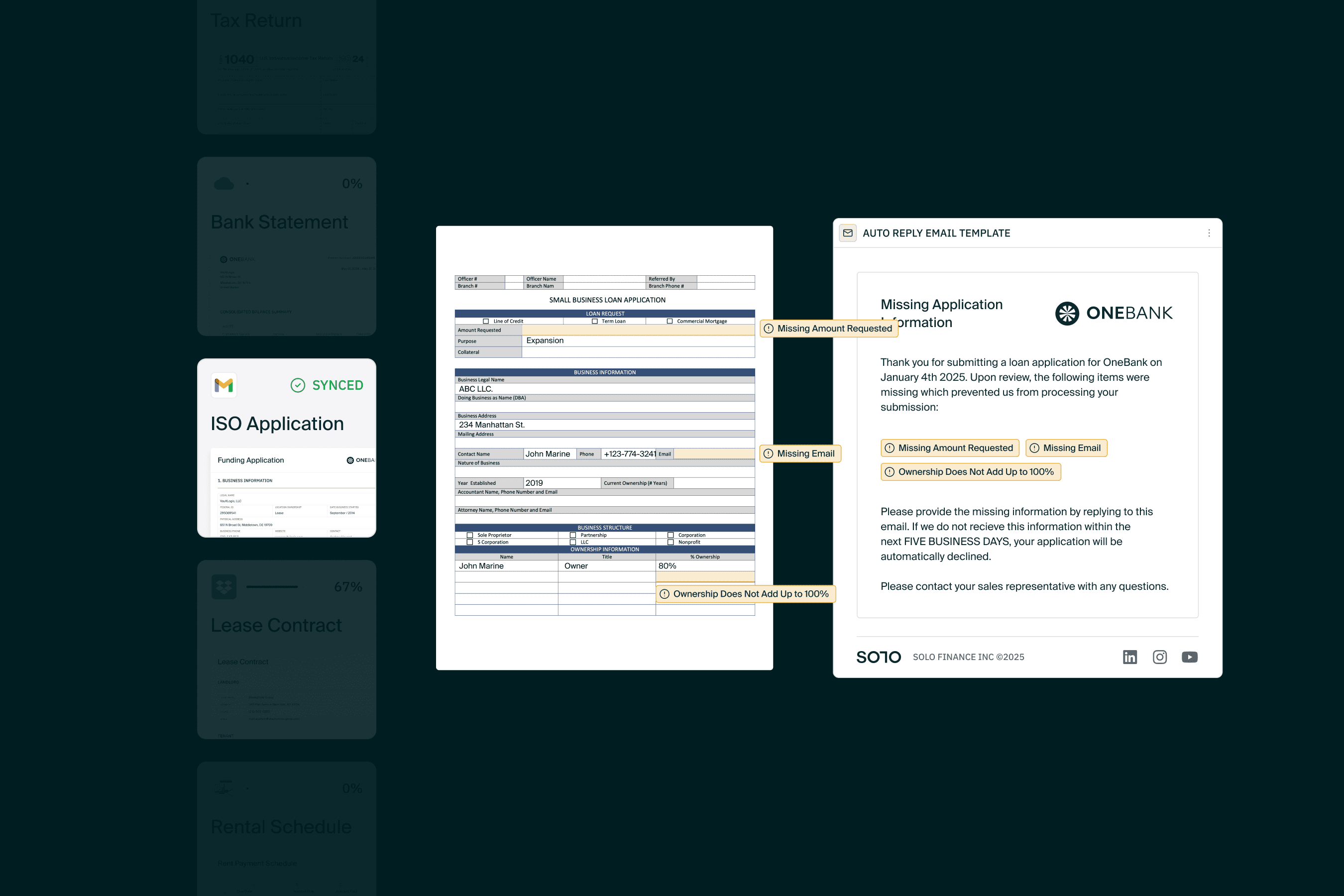

The legacy loan origination process can be as long as 60+days depending on the size, complexity, and the use of the loan. This is especially true for complex business loans like the SBA guaranteed loan.

1. Loan Inquiry

The process begins when a borrower expresses interest in obtaining a loan. This could involve discussing loan options, terms, and eligibility requirements with a lender or initiating an application online or in-person.

2. Application Submission

The borrower submits a formal application, providing necessary information such as:

Personal or business details.

Financial data (income, expenses, assets, liabilities).

Purpose of the loan.

Supporting documents (e.g., bank statements, tax returns, credit reports).

3. Document Collection and Verification

The lender collects and verifies the provided documents to confirm the accuracy of the information. This includes:

Checking the borrower’s identity.

Validating income sources.

Ensuring all required documentation is complete and correct.

4. Credit and Risk Assessment

The lender evaluates the borrower's creditworthiness and risk profile using various tools:

Reviewing credit scores and credit reports.

Analyzing financial statements and cash flow.

Assessing collateral, if required.

5. Underwriting

Underwriting is the process of evaluating whether the borrower meets the lender's criteria for loan approval. This is often the most document heavy step used to:

Analyze the borrower’s debt-to-income ratio.

Assess repayment ability.

Apply the lender’s internal risk models or automated underwriting systems.

6. Loan Decision

Based on the underwriting results, the lender decides whether to approve or deny the loan application. If approved, the lender determines the loan amount, interest rate, and repayment terms.

7. Loan Approval and Offer

The lender communicates the decision to the borrower, presenting them with an official loan offer (term sheet). This document outlines:

Loan terms (interest rate, tenure, repayment schedule).

Any conditions for approval.

8. Loan Acceptance

The borrower reviews the loan offer and, if acceptable, signs the agreement to proceed. Any additional requirements, such as paying fees or providing final documents, are completed at this stage.

9. Disbursement

Once all conditions are met, the lender disburses the loan amount. Funds are transferred to the borrower’s account or directly to vendors (e.g., for home or car purchases).

10. Post-Origination Management

After disbursement, the lender continues to manage the loan through servicing activities, including:

Payment collection.

Monitoring repayment performance.

Addressing any delinquency or default issues.

Learn how to use SOLO 01 PULL to revolutionize the loan origination process, streamlining the loan origination process from months to minutes.