Index

CATEGORY

Best Practices

SOLO for Commercial Loan Origination Systems: Unify Siloes, Route Deals, Eliminate Manual Data Entry

Nov 15, 2024

SOLO is a data ingestion platform transforming how data is collected and activated for banks and lenders.

Often used throughout the loan origination, underwriting, and closing processing, SOLO unifies data siloes and eliminate the need for manual data entry from documents and CRMs into credit workbooks, specialized LOS systems, and across the operating tech stack throughout the loan origination processs.

How? Customer data portability.

Data Portability for Commercial Loan Origination Systems

SOLO replaces the need for additional Loan Origination Systems by ingesting a customer's data once, turning it into a reusable "record of truth" per consumer.

The record can be used to structure and restructure data to route seamlessly across the systems where its needed, automatically. Banks query the data they need in real time, optimizing both efficiency and customer experience without needing to re-key data into new systems.

The goal: a full 360* view of customers at all times across the entire tech stack. Without the need to re-submit requests for personal and financial information to a new system for every product in the portfolio.

This guide provides a comprehensive overview of using SOLO as the data portability layer for commercial loan origination systems.

Commercial Loan Origination Systems: Why Are There So Many?

A Commercial Loan Origination System (CLOS) is a software platform designed to manage the entire loan origination process, from initial customer application to loan disbursement.

Over time, new tech vendors have introduced a new CLOS for every product in the bank with a goal to streamline the lending operations on a loan by loan basis.

This has sped up some pieces of lending decisions and loan origination in the short term, if you look at each product in its own vacuum.

The problem? With every new platform, banks introduce a new data silo.

Redundancy after redundancy as underwriters, loan processors, and relationship bankers are locked into processing documents and customer information from system to system.

On the line: customers are forced to go through another loan origination system every time they need a new financing option, even if their relationship and all their information is already with the bank.

What the ecosystem has created is not a data scarcity issue. Now, underwriters and loan ops are forced to work around a number of data bottlenecks that limit how seamlessly and proactively bankers can scale credit relationships.

How Lenders Use SOLO as a Data Portability Layer for Loan Origination

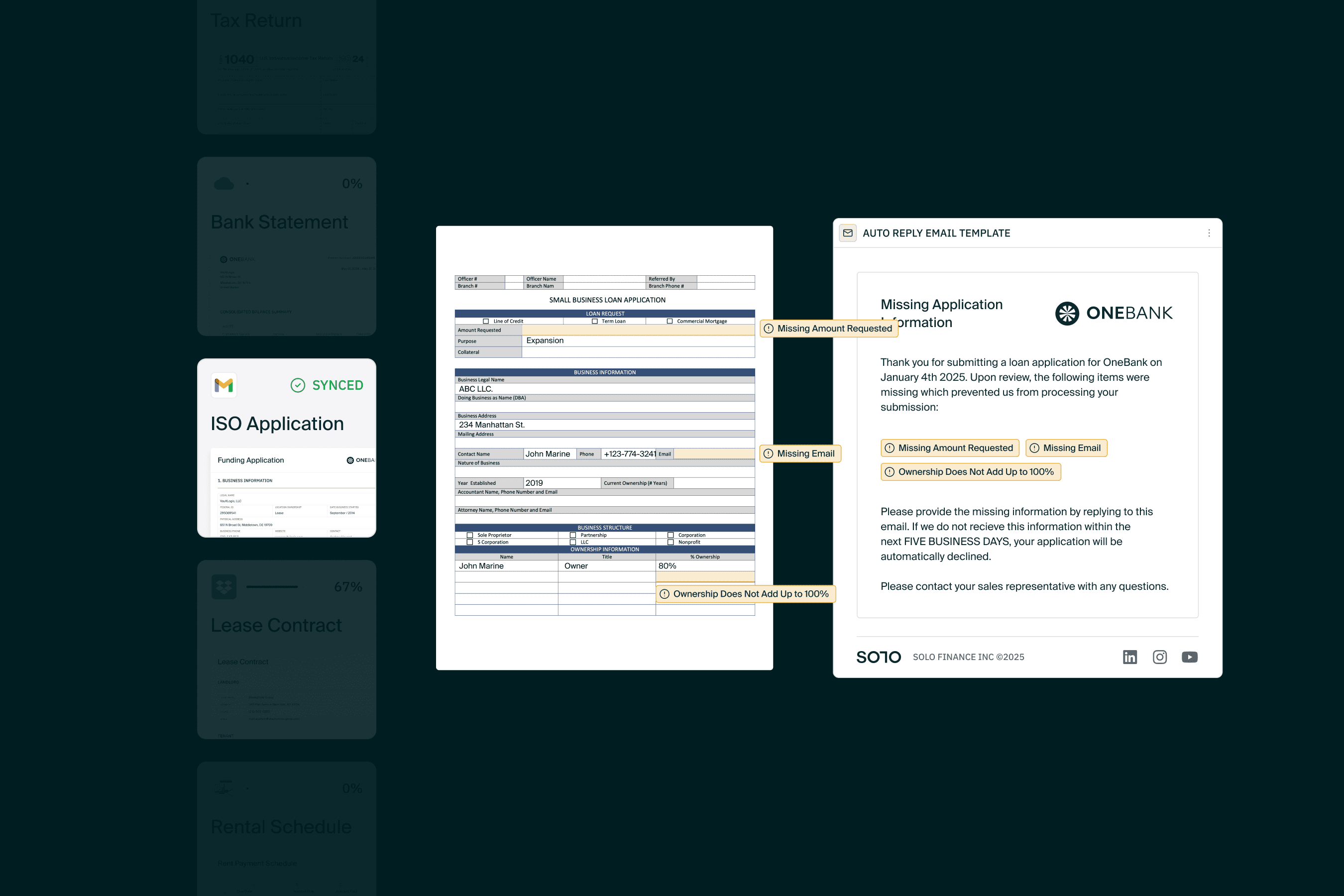

01 PULL is SOLO’s solution for lenders transforms data collection so that data becomes usable at first collection point for every part of the lending tech stack. How it works:

Frictionless Data Collection: the PULL platform’s borrower onboarding portal makes customer data collection seamless with the option to upload files directly in a secure loan application.

Lenders build their custom application using PULL’s drag and drop editor. No code required. SOLO powered applications can be embedded to existing website pages or hosted by SOLO.

SOLO-powered loan applications can process any document a lender may require for underwriting a loan application: bank statements, tax returns, contracts, lease agreements, promissory notes, etc.

Borrower Data Ingestion: Borrower information is distilled into raw data points, then rebuilt as a real-time ledger, calculated to the lender's requirements, so data is re-structured into a dynamic record that is ready to sync into any system.

Run any number of reports on a single customer record to automatically create real time structured data sets formatted to sync to each of your systems, proactively.

Automated Underwriting: Once borrower data is mapped into a report, SOLO gives your lending department the power to sync directly into your underwriting spread, or route borrower data to any number of relevant commercial loan origination system using configurable pre-screening logic.

Pre-screen borrowers, proactively underwrite to every relevant product in the spread, and preserve borrower data in a record that can be used again and again across every system.

Stay Synced and Continuously Underwrite: Proactively match borrowers to products as their business grows. The SOLO platform enables lenders to continuously underwrite the full picture of a borrower’s financials in real time, for every product in the matrix, all from a single application.

No more LOS siloes, just a single data collection point that makes data usable for every part of your tech stack.

SOLO for Loan Origination Systems: Results

01 PULL from SOLO One enables banks, credit unions, and lenders to turn data collection into a competitive advantage, enabling lenders for loan origination growth without ripping out current systems by introducing:

Scalable Underwriting Power

Unified Data Silos

Improved Customer Experience

Increased Lifetime Value

Implementing SOLO With a Commercial Loan Origination System

SOLO provides lenders with hands on support prior to and throughout implementation of 01 PULL as a data portability layer for commercial loan origination system.

Our process is developed to efficiently gauge a lender’s potential optimization through SOLO prior to fully adopting the commercial loan origination system.

Discovery: demo the platform and review your unique underwriting process with SOLO engineers.

Data Test: sample SOLO’s capability for out of the box functionality and identify need for further customization.

Proof of Concept: Assess SOLO’s workflow using your data, your process.

Implementation: SOLO develops your environment, trains essential team members, and integrates to essential systems.

Monitor and Optimize: Continuously monitor the CLOS system's performance and refine processes as needed to enhance functionality.

SOLO for Loan Origination: Turn Data Collection Into A Competitive Advantage

Make Data Collection A Competitive Advantage. Transform a single application into an ongoing record of truth for every customer. Continuously underwrite the full picture, for every product in your matrix, all from a single application.