—

(n) information that a borrower voluntarily provides or grants access to during the loan application process. This data is shared with lenders or third-party platforms to facilitate underwriting, risk assessment, and loan decision-making, while ensuring transparency and borrower consent.

Customer permissioned data sources for loan underwriting can include everything from financial accounts to customer relationship tools, like Salesforce and Hubspot, to paint a full picture of who a

Key Characteristics:

1. Borrower-Controlled: The customer explicitly authorizes access to their data, such as financial records, credit reports, or banking information.

2. Specific Purpose: The data is shared for specific purposes, such as verifying income, assessing creditworthiness, or analyzing cash flow.

3. Transparency: Borrowers are informed about what data is being accessed, how it will be used, and with whom it will be shared.

4. Revocability: Borrowers can revoke permissions at any time, limiting further access to their data.

Examples in the Loan Application Context:

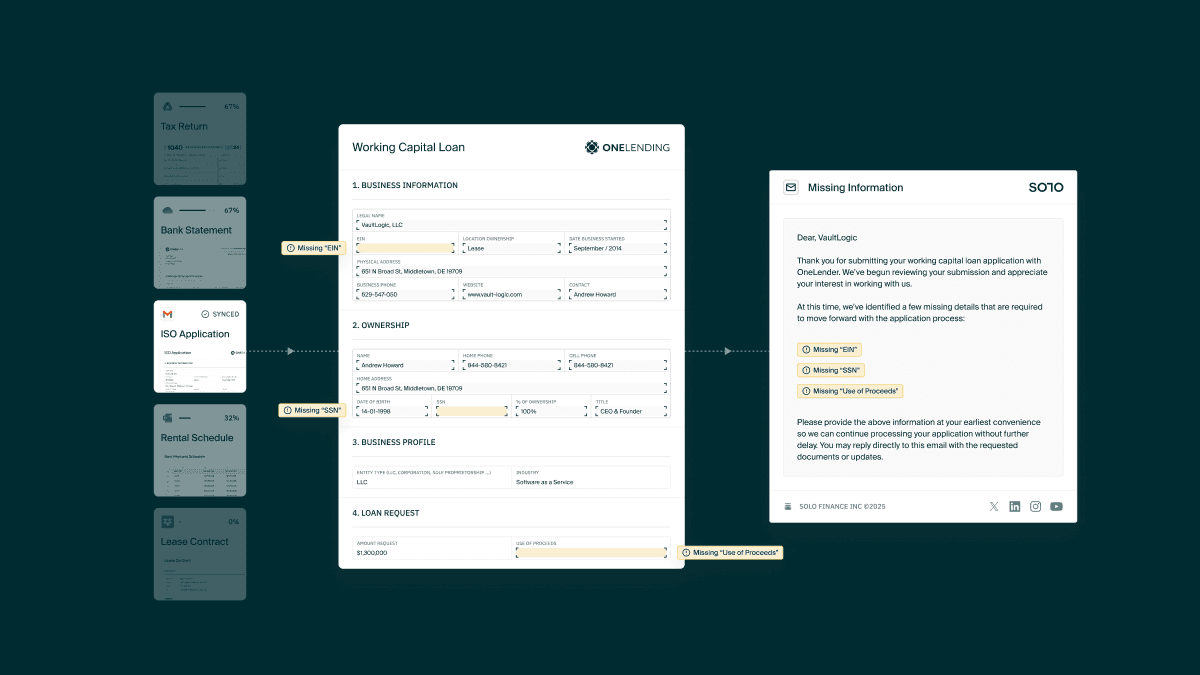

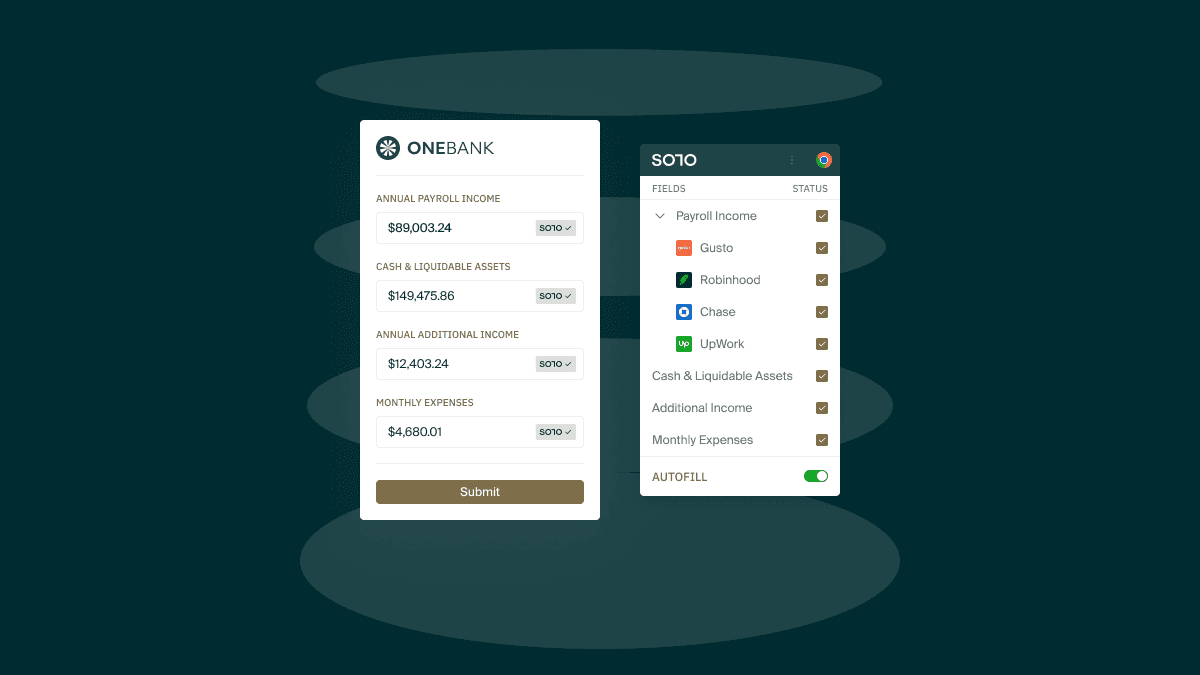

- Bank Account Access: Customers grant lenders read-only access to their bank statements through platforms like Plaid to verify income and spending patterns.

- Tax Records: Borrowers may allow direct retrieval of tax returns via systems like the IRS Data Retrieval Tool.

- Employment Verification: Borrowers provide access to payroll systems or employment records for verification purposes.

In addition to maintaining compliance in the open banking era of CFPB 10333, customer permissioned data sources can also be key to facilitating a high conversion borrower application as discussed in our high conversion digital lending master class.