From the Dinner Series: Is Credit Overdue for an Unbundling?

Hot Takes from the SOLO Credit Dinner Series II: Lending Pessimism, The Unbundling of Credit, Restructuring Credit Product Strategies, and Why It All Circles Back to Trust.

Hot Takes from the SOLO Credit Dinner Series II: Lending Pessimism, The Unbundling of Credit, Restructuring Credit Product Strategies, and Why It All Circles Back to Trust.

Like many of you, our team spent the week with banking and fintech’s finest at Fintech Meetup in Las Vegas, NV. On night one, we were privileged to host a dozen bankers and credit experts alongside our friend Alex Johnson, Founder of Fintech Takes, for the second installment of our Credit Dinner Series.

Closed door conversations remain my favorite because the unfiltered takes on credit tend to be the ones that we all know are true but can’t always say out loud.

I won’t go into all the specifics, but here are a few of the main themes that came up around the table last week.

It’s not surprising that many of us are weary of the financial landscape for lending and credit products, given what we hear about the current environment.

There is a lot of generalized uncertainty, even though many of the fundamental facts haven’t changed all that much.

I was a bit surprised by this pervasive attitude that credit is in a slump. I don’t think the customer appetite is gone. I think maybe it’s our predominant approach to how credit is understood and offered that fuels the real problems. Which led us to…

Alex and I have bonded on this point quite a bit, although it’s not always the most popular with more…"traditional" risk leaders.

Hot Take: We need to unbundle the credit landscape.

We’ve overstandardized in two ways, for:

Alex shared great insight over dinner on why consumers are actually in a credit slump, and it might have more to do with their options than their spending.

Credit products are, by design, propping up a system that self selects for failure in the modern world. Younger people have financing options for all the things their parents and grandparents wanted, and their unwillingness to buy into those same financing agreements may not be a true indicator of their creditworthiness or the health of credit at large.

Example, why are we pushing mortgage lending as an overall indicator of financial maturity and success when fewer and fewer young Americans cite that owning a home is not a main financial goal in the next 5 years?

There are a number of overarching factors that have swayed consumers away from legacy products. Banks don’t really acknowledge that as quickly as they should, if at all.

However, the credit leaders that learn to invent in real time for their customers are going to come out on top. New best practices in data collection, activation, and sharing will be the key that unlocks their ability to do so.

I’ve said this a million times, but overstandardization of data is the other piece of this puzzle and will be the death of good credit.

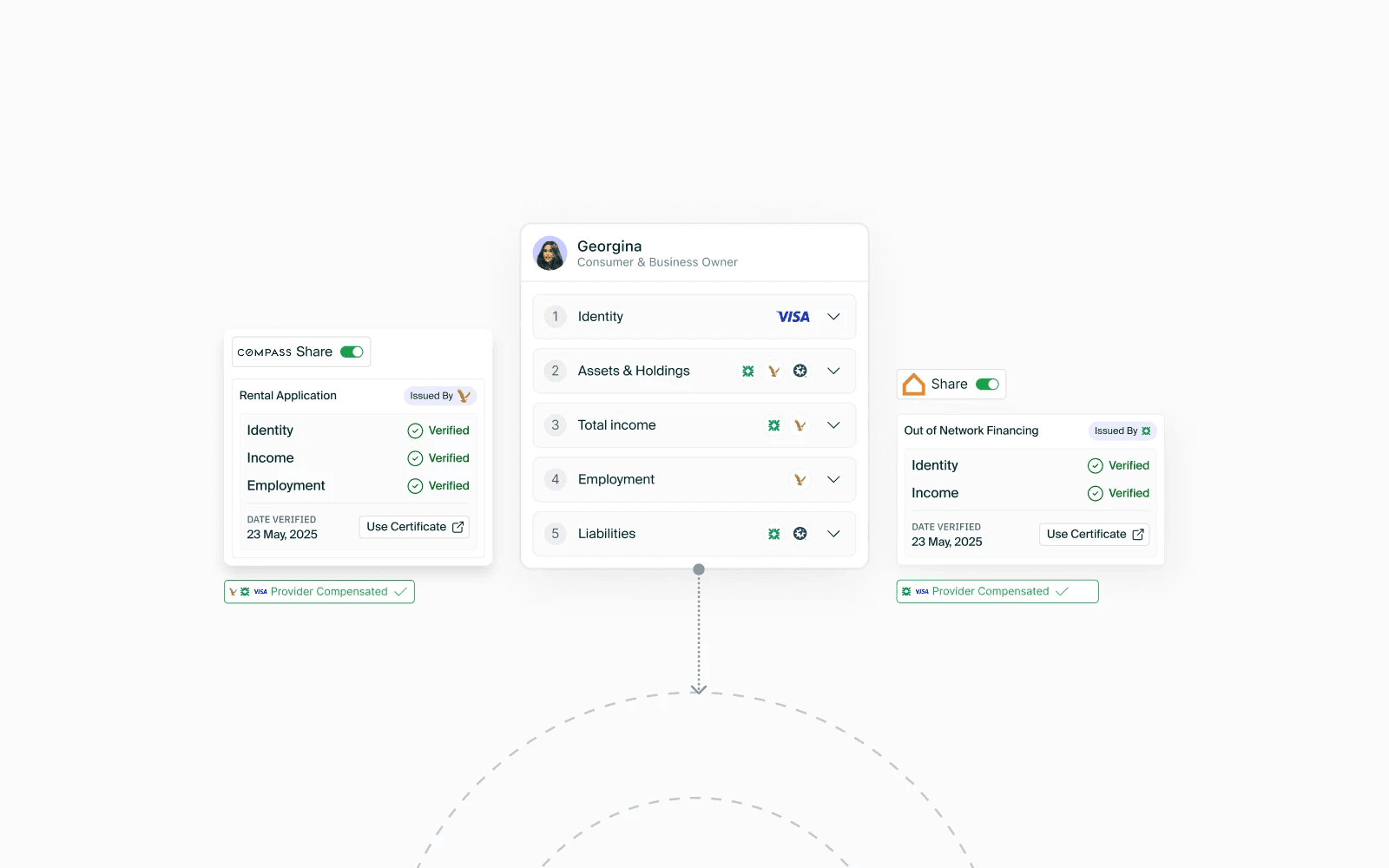

The new age of banking relationships is not going to be fueled with a single credit score or a new score building tool, but with permissioned data that actually unlocks a better outcome for our end customer.

Imagine if you could submit one application, and see every option for you at a bank, continuously. And, imagine if your banker was able to automatically reach out with new offers, customized to you in a transparent process you understand, based on your financial progress.

This is the type of credit data relationship we see fueling a restructuring of core product offerings. With the vast amount of dynamic data that can now supplement incumbent ways of thinking, you can design credit to fit your customer today and evolve with them for the future.

If your customer can connect their systems of record, and provide all their information once to constantly be in sync with your systems, there is no reason automation cannot one day facilitate hyper-personalized, low risk credit products with the speed, efficiency, and assurance that banks and lenders need to constantly deliver the actual financing needs of their customers. You can get started right now, actually, with SOLO.

The major caveat being that you must have healthy data governance and best practices that account for quality decision making, not just faster decisions (I have to add this as a former data scientist for all my fellow risk and data leaders in the room, and don’t worry this is our forte).

The big takeaways: Legacy credit metrics and products were not designed for 2025. It’s no shock our modern world doesn’t take to the old systems the way it once did. But if we want to move forward in creating an ecosystem that one day supports bespoke credit products for every individual and business (my dream by the way), it starts by careful design of the data collection and sharing processes that power the future of lending.

And finally, we talked about how we’re all talking to each other.

My own pet peeve lately, and one we discussed at dinner, is the polarizing approach society has taken to talk to customers about their financial goals.

Customers have gotten used to being kept in the dark on credit, and then ‘scolded’ by the general public for their financial goals. But TLDR: shaming people for regularly buying avocado toasts is not going to solve slow turns in mortgage lending the same way shrouding credit scores in secrecy won’t actually stop people from trying to ‘game’ the system.

Imagine if instead of judging our customers for their goals and trying to fit them into the credit box we’ve always known, we create that context aware, bespoke system previously mentioned that allows for customers to have agency over how they leverage their own creditworthiness to fund the goals that matter most to them.

Proving themselves as good creditors and partners in the process.

This really isn’t a foreign concept. Meeting the customer where they are is relationship banking at its best. And if we want to be the best at financing relationships, we have to listen and offer back (with good judgement) what our customers actually need in the context of their life.

It comes down to a few simple things.

Credit relies on trust.

Trust is built on relationships.

Automation can return relationships, and therefore trust at scale.

And the right approach to data collection, activation, and sharing powers automation that reliably reshapes the future of credit for us all.

Maybe not so hot of a take after all.