BlogOct 20, 2025

Solutions

© SOLO FINANCE INC. 2026

Aligning Credit, Customer Acquisition Strategy, and Customer Experience for Strategic and Scalable SBA Loan Originations

I spent the last couple of years prior to SOLO on an SBA and USDA lead generation team at a community bank, scaling SBA and USDA loan originations through digital strategies. Any government guaranteed lending team already knows what I learned there:

It’s really difficult to originate GGL loans. Especially in the digital landscape of quick financing with same day delivery, where borrowers can (and do) apply to 10+ lenders at once and accustomed to seamless, digital experiences.

Our team gained a lot of insight over the course of many, many ad experiments. The biggest key to originating new SBA and USDA loans (without a broker) lies in a strategic middle ground between credit appetite, ad strategy, risk tolerance, and underwriting experience.

If I were planning to scale SBA loan originations this year, here’s how I’d start again.

A commercial banking team that keeps saying, "we'll fund any small business this size, region, etc just bring me leads" is setting up a failing strategy.

Being industry agnostic is not the problem. The issue is that a lack of focus and messaging clarity will cause your strategy to fall flat in a sea of digital competitors.

This may sound very obvious, but it's more common than you think to find marketing teams with little to no clear direction on the bank’s GGL lending strategy. And, to find marketing teams developing their own ICPs that can be reached easily on digital channels, but that Credit and BDOs don’t actually want leads from.

Consider your team’s current approach. Does your content just introduce the SBA loan? Or are you showcasing its impact for ‘this industry’ with ‘that’ use case, making a clear case and pointed case for the SBA's unique deal structure in your borrower’s unique context? Can you demonstrate the SBA loan’s impact for a business owner with a specific type of business over time?

Example: we did this once in a website article by modeling out a hypothetical business acquisition in a target industry using SBA loans vs. Term Loans to show how the SBA deal structure impacts cash flow.

TLDR, a visualization and deep dive into the estimated cash flow the SBA loan freed up month to month for our target type of business was an incredibly effective tool.

Unsurprisingly, it was our highest conversion website content for originating SBA leads organically.

We could not have effectively launched this campaign if we only had generalities to work with from our credit team.

I recommend teams create a few target segments based on the current state of the portfolio. What deals are you currently funding successfully? What profile can you create from those? Segment by region, industry, and most of all SBA use case.

One of my best tips for Marketing teams: read as many credit memos as possible as you’re building out your ICP and messaging around use cases that will resonate with each. The "Use of Proceeds" section on SBA credit memos will be an incredibly effective tool for guiding a "Use Case" focused content strategy.

Specificity in audience, target, and use case is a secret weapon.

The best loan origination strategies identify the overlap between digital acquisition efficiency, underwriting complexity, probability to close, and default data.

If you can get Credit, Digital, Sales, and Risk in a room, start by having a conversation.

Outline the go/no goes criteria and any known ideal borrower types. Then, take those characteristics to your Digital team. Have your keyword specialist check keyword targets that would be used to reach your borrower through Organic + Paid channels.

With this quick test, your team will be able to reveal high level insight into search intent, digital competition, and difficulty with market penetration to help understand what your borrower in that segment actually needs from online financing resources.

And, you’ll start to understand which borrowers are going to have high CAC, and which can be earned through organic efforts (with some paid backing if you need immediate results, right now).

For example, if you're looking to finance medical practices you might have a much harder time reaching them without a big paid budget + precise targeting because of keyword competition and overlap into consumer searches. Even with targeting and budget, you may struggle to land in front of the right person.

We actually tried this in the past.

Most of those searches to optimize for were split between independent physicians looking for financing solutions and patients looking to refinance medical bills.

From these insights, we knew to keep trying for medical practices but reframe our language to better target an independent physician vs their patients (target for the terms private practice financing vs medical loan).

We also knew they probably wouldn't be our very best performing target on digital channels within the budget, time frame, and loan size we wanted to optimize for.

So we pivoted to an industry that our credit team would approve and had clearer search intent, within a clear B2B target that wouldn't be competing (even unintentionally) with consumer searches, and had a positive trajectory but was not overly competitive with results.

That became a high performing ICP segment much faster through channels that cost us less. It was segment we could consistently reach, and Credit would reliably want to fund.

Marketing teams have the very best resources for high performing loan origination campaigns and nurture sequences in their own offices.

SBA underwriting is a notoriously difficult process for borrowers that prevents them from applying in the first place.

Borrowers stare down a laundry list of documents on top of day to day of actually running a business. And I guarantee you they turn to google for help...do some quick keyword research and you'll see what I mean.

That should signal to banking teams to create a differentiator via their experience: if they can solve for this very clear and very known SBA loan application pain point they will win the market with speed, efficiency, and borrower appreciation.

At the time, our patched together solution for nurturing leads through the SBA underwriting process was to work with our underwriters to create custom resources around the pain points they see every day.

We published more detailed content around the underwriting process at our specific institution to reach our audience in the ‘research’ stage, which often out performed the ‘fluff’ online.

We also created as many templates as we could to provide to borrowers during and before the application process to support them through the paperwork heavy SBA loan process (although it was still on our borrowers to complete and submit the paperwork before our underwriters then had to process each document- and that was a huge roadblock to our ability to scale SBA loan originations).

I frequently think of these missed opportunities created from the paperwork burden of an SBA loan application.

Our marketing team would spend significant time and resources getting SBA loan leads into the bank’s ecosystem, but when it came time to submit underwriting paperwork, many leads would drop off. They either,

This is the piece of the puzzle where I predict the best lenders will embrace new solutions to win the SBA market.

How much better of an experience would it have been had we been able to provide our borrower their financials and documents upon application, instead of underwriters having to hunt them down and trace back every calculation?

It would have been incredibly costly at the time. We would have needed significant head count and expense, essentially hiring a separate accounting team just for potential leads (which was not quite in budget).

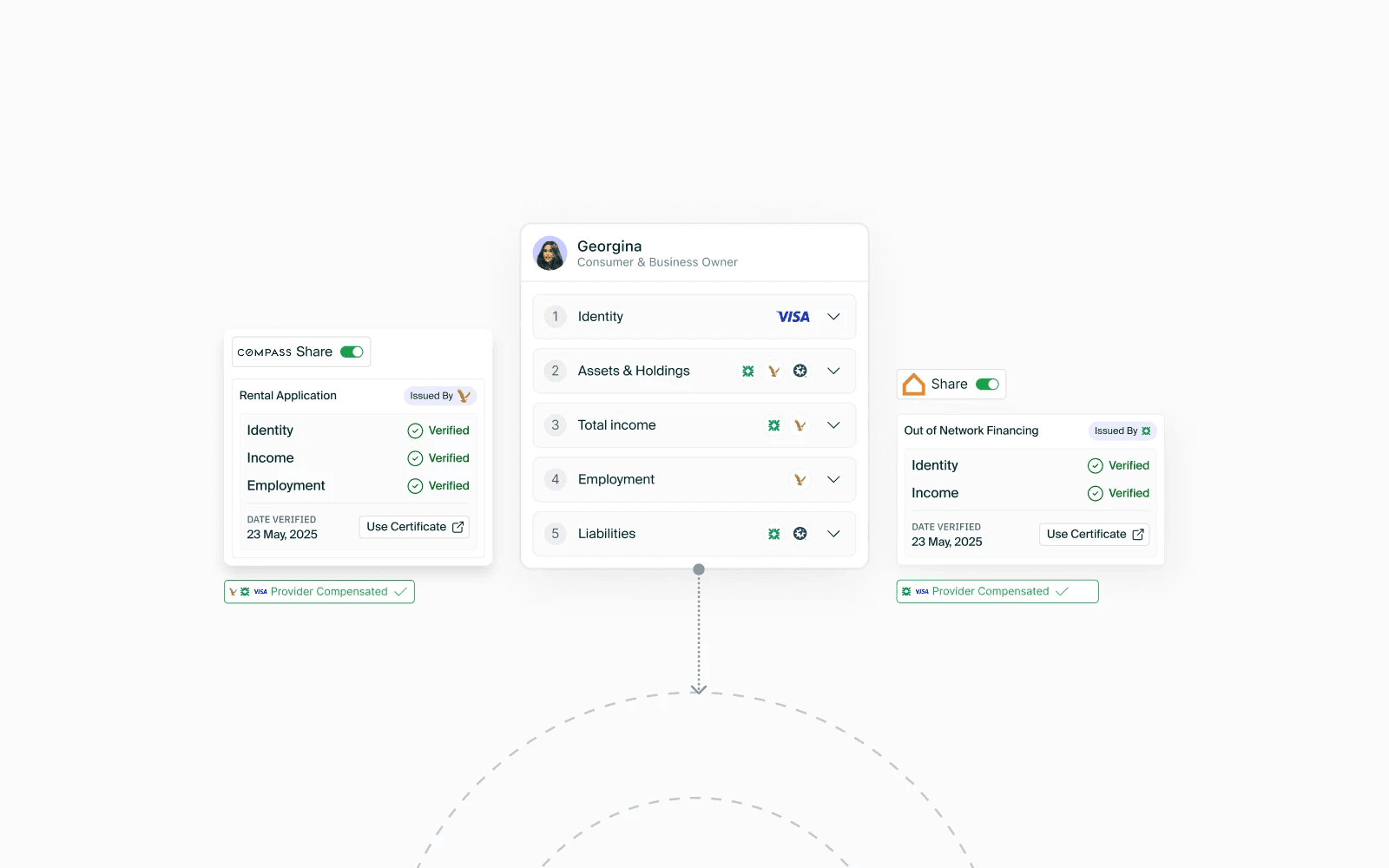

But this is precisely the problem we’re solving at SOLO for paperwork heavy loans like the SBA 7(a) Loan, USDA loans, and other government guaranteed programs, by fostering a new level of collaboration that connects onboarding to underwriting and helps the borrower 1.) immediately understand their options today, creating all their application documents for them in the process while 2.) guiding them towards eligibility in the future, with real, actionable, and transparent steps forward to keep them engaged.

Which leads me to what I predict is the future of scaling SBA lending in 2025 and beyond.

A core piece of SOLO’s digital onboarding solution is the ability to generate all a customer’s loan application documents for them according to their lenders logic, from just their application.

Applied to the SBA loan origination process, SOLO can be used to create any and all SBA loan application documents on behalf of the borrower, in SOP compliant formats, using the customer’s data from both account integrations and uploaded documents.

This piece alone will be revolutionary for conversion rates on both paid and earned lead generation. But what I’m even more excited about for transforming the SBA landscape (particularly for Small Loans) is the SBA Borrower Portal and Roadmap SOLO creates for borrowers who may not meet SBA eligibility requirements today, but have potential to in the future with guided support.

Not just process automation (although it does that too), SOLO’s SBA platform creates more borrowers by guiding towards eligibility with continuous underwriting through your lens of credit. Borrowers get personalized next steps to meet a lender’s internal credit policy and SOP detailed requirements, and their documents stay updated in real time as their financials change. Imagine, choosing between ten lenders: nine that leave you to fend for yourself, and one that is a clear partner like this in your road to financing?

The SBA 7(a) process is painful but it doesn’t have to be. If anything, it creates a very immediate untapped opportunity for banks and lenders to stand out in the sea of competition is through their application to funding experience. Lenders can stand out by changing the status quo:

As banking (and credit tech teams, in my case) we strengthen both the SBA and the borrowers they serve by:

We're all in this field because we care. And we all hope to make programs viable and attractive to everyone involved on the deal.

The better we do as marketing, credit, and lending teams at making the SBA programs discoverable and accessible, the more chances business owners have to succeed with financing that lets them be strategic about how they grow and the opportunities they take.

When it's all grounded in this mission, your strategy will show and your borrower will experience what it’s like to work with an institution that treats them as much like a neighbor as a customer. I think that's the real heart of programs like these, and where technology should step in to make the original intent of the programs scalable.

Out of all the things to scale, this type of personalized service made possible with tech like SOLO is one I hope we’ll lean into to transform the SBA landscape in 2025 and beyond.