BlogOct 20, 2025

Alex Johnson, Fintech Takes, dives into the biggest questions on the future of data sharing, credit, and information asymmetry in financial services through the lens of SOLO's network model.

In recent years, open banking has added APIs, alternative data, and automation. Yet, the core process of collecting and trusting information still looks much like it did decades ago.

Why? And what can be done to reshape that process in a more fundamental way?

Introducing Source of Truth a new podcast series hosted by Alex Johnson, Fintech Takes, to dive into the biggest questions on the future of data sharing, credit, and information asymmetry in financial services through the lens of SOLO's network model. Listen to all four episodes here, or wherever you get your podcasts.

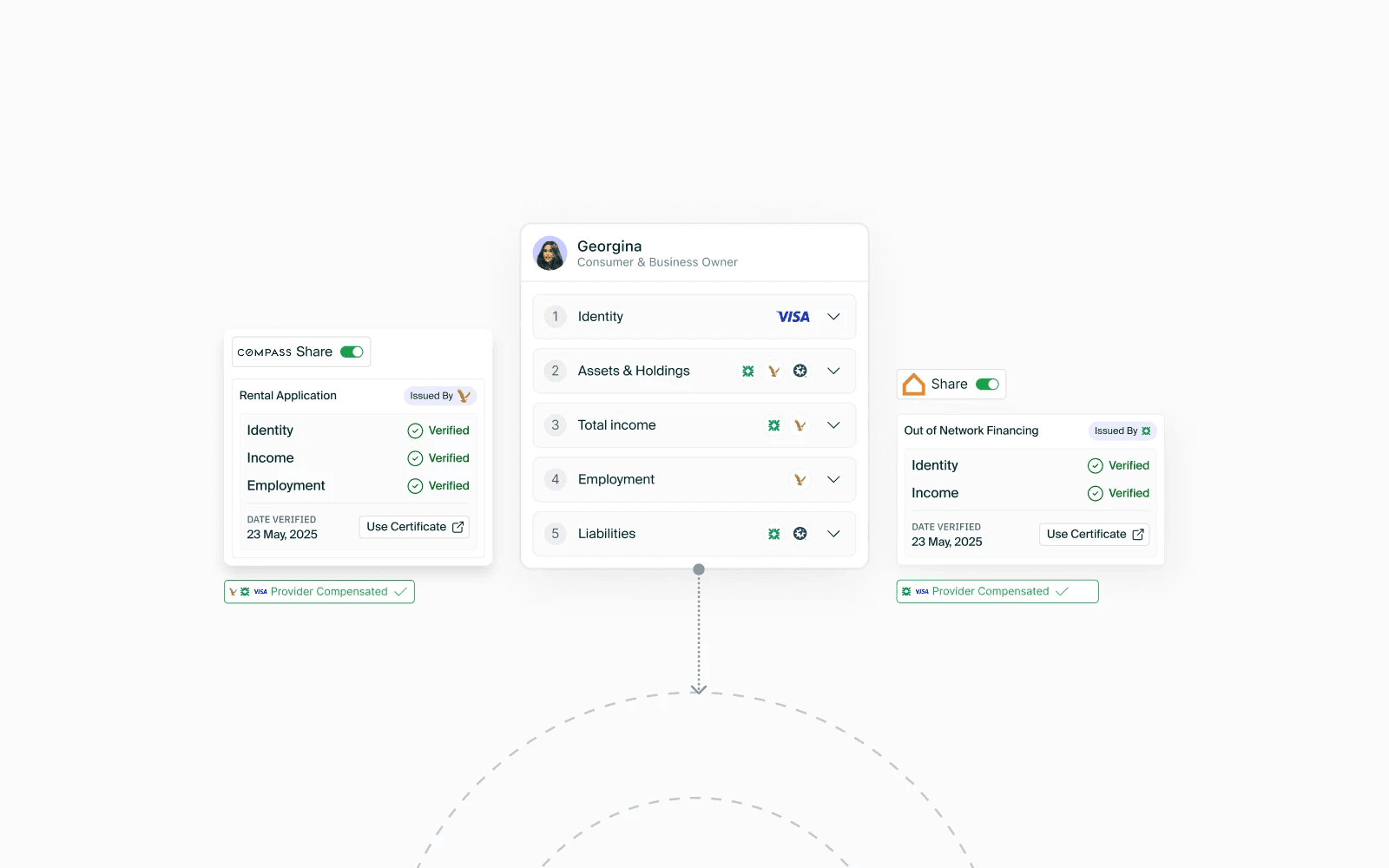

In Episode 1, Data Scientist and SOLO Founder, Georgina Merhom, unpacks how lending data is collected, verified, and (too rarely) reused throughout the financial services ecosystem.

Highlights:

Georgina details how SOLO has spent the last two years making customer data portable across institutions, work which made clear that there's an overlooked architectural flaw in open banking: Most financial data today is collected in a way that cannot be reshared, and it's breaking the collaboration that should define open banking's future.

The current system collects and stores data to fit APIs but not to grow trust. Data provenance is lost, sources can't be trusted, validation disappears, a 'reset' occurs. Again, and again, and again.

This opening episode tees up the larger theme of the series: building systems that don’t just capture truth but create trust.

The standardization of data outputs, which confuse assessment with 'truth' costs borrowers and lenders a critical asset: context.

Martin Kleinbard, former CFPB Staffer and Fintech Operator, joins for Episode 2: Context is King.

Highlights:

This episode explores what happens when we reduce everything to a single number: lenders miss nuance, consumers get misread. A credit score can predict repayment, but only context explains it.

And in the end, context is king.

In small business lending, true data portability is never as simple as an API connection. The guests on Episode 3 of Source of Truth know that all too well — and are bringing the unfiltered insight to prove it.

These conversations are short but illuminating: expect war stories from the early days of well-known fintechs, insights for scaling up in our heavily regulated industry, and candid thoughts on what the industry needs next.

Listen as Alex Johnson unpacks what these hard lessons tell us about the future of lending and data infrastructure in the U.S alongside four veteran founders and fintech operators.

Guests (in order of appearance):

Episode 3 is your field guide to the real constraints operators face — and the data standards and product choices that actually moved loss curves, conversion, and access.

What would open banking look like if it was re-engineered from the ground up, knowing what we now know?

In this final episode on data portability in financial services, Alex is joined by Eric Woodward, former President of Early Warning and one of the key architects behind Zelle’s Risk Service.

Eric and Alex zoom out to the system level: who controls financial data, who pays for access, and what a healthier network for open banking could look like.

If we could wave a magic wand and start with a blank sheet of paper, how would we design data infrastructure (drawing from the lessons learned by credit bureaus, open banking data aggregators, and industry consortiums) to actually work best for the ecosystem?

Highlights include:

Consumers in control. Furnishers compensated. Shared rules. Trust incentivized by design.

“I’ve been watching SOLO build toward this network launch for the last year. What gives them the right to win is simple: they’ve unified messy, disconnected customer data into a portable trust layer — live today, even at institutions with some of the lowest technical maturity.”