BlogOct 20, 2025

The Verdict: Open Banking Can’t Afford Another Patchwork 1033. Watch the Town Hall with Founding CFPB Member, Former CFPB Staffer, and Industry Advocates.

When the Consumer Financial Protection Bureau first proposed its rule under Section 1033 of Dodd-Frank, the aim was deceptively simple: give consumers greater control over their financial data. Nearly a decade later, the future of open banking seems more vulnerable than ever before.

At SOLO’s recent Open Banking Town Hall, open banking experts offered a proactive vision for what 1033 could look like through the lens of the policy makers responsible for the law’s origins: a future for data sharing where responsibility is tied to the transaction, not the institution, and where consumers remain in perpetual control of their data.

The discussion on Section 1033 could have been another rehash of banks versus fintechs. Instead, it revealed a surprising amount of convergence—paired with some nuanced debate—on what it will take to chart a more permanent future for America’s open banking system.

Watch the full discussion, straight from The Source:

Panelists:

The panel on Section 1033 at last week’s town hall could have easily fallen into the familiar rut of banks versus fintechs. Instead, it revealed something more useful: everyone agrees the current data-sharing system is broken. Where the decisions still to be made will determine how we rebuild it.

SOLO’s panelists went straight to the source of those who know the policy and history of the CFPB best to offer unique insight on the path forward.

Jim McCarthy, one of the CFPB’s earliest architects, warned of repeating the sins of the credit bureaus—hoarding consumer data and monetizing opacity, “Eighty percent of complaints in the CFPB’s database are against the credit reporting companies. Let’s not recreate that model.”

Phil Goldfeder of the American Fintech Council pushed for industry-led standards, forged in collaboration rather than imposed by any one party, “If the government is doing it for the industry, you’ve lost. If one sector of the industry is doing it, you’ve lost. It only actually works if you’re doing it together—otherwise it won’t last.”

And Martin Kleinbard, with one foot in regulation and another in fintech operations, clearly framed the issue: rules shouldn’t be written by company type at all, but by role in the transaction. Whoever adds trust, lineage, or compliance value should be compensated; raw data alone should be near free. Martin’s take on the core design flaw of the current rule: “The original 1033 wrote duties based on the company vertical. In reality, we all wear different hats. In every transaction there’s a sender and a receiver. Sometimes they add value, sometimes they don’t. The rules should follow the role, not the company label.”

The path forward for 1033: a system that addresses where the original rule missed the mark on frameworks for the proper governance, economics, and technical architecture of open banking.

An overarching theme posed by the questions in recent CFPB 1033 ANPR: who is responsible to the consumer, and to what extent should the burden of regulatory oversight be shared by the players who profit from open banking?

McCarthy pointed to the billions banks have poured into compliance infrastructure as a form of trust that can’t simply be handed away to the third parties who currently rely on it to power their business model at an essentially subsidized cost.

Governance that ties accountability to the parties responsible for creating and maintaining trust—whether bank, fintech, or otherwise—is the only way to prevent a repeat of the credit bureau failures that dominate the CFPB’s complaint logs.

The panel’s sharpest exchange came when our panelists were asked if banks should be able to charge for their data. Kleinbard advocated for a distinction between raw data, and data that’s been endowed through the work of institutions with trust: “If it’s just raw data, it should essentially be free. If you’ve actually added value—lineage, fraud analysis, underwriting—then you should be compensated.”

Goldfeder was quick to add that consumers will accept such a model if it’s transparent: “If the consumer recognizes the value-add of each party, they’d agree there should be some mechanism for compensation. It’s complicated, but the system can’t be burdened by any one company.”

This is the fulcrum of the economics debate: will open banking incentivize sharing or hoarding? Kleinbard explains, “If we had started out with a value-add framework where all the players in the ecosystem understood that when they added value they were compensated for that and when they were receiving value they were paying for that… it would have become a much more expansionary ecosystem rather than a zero sum ecosystem.”

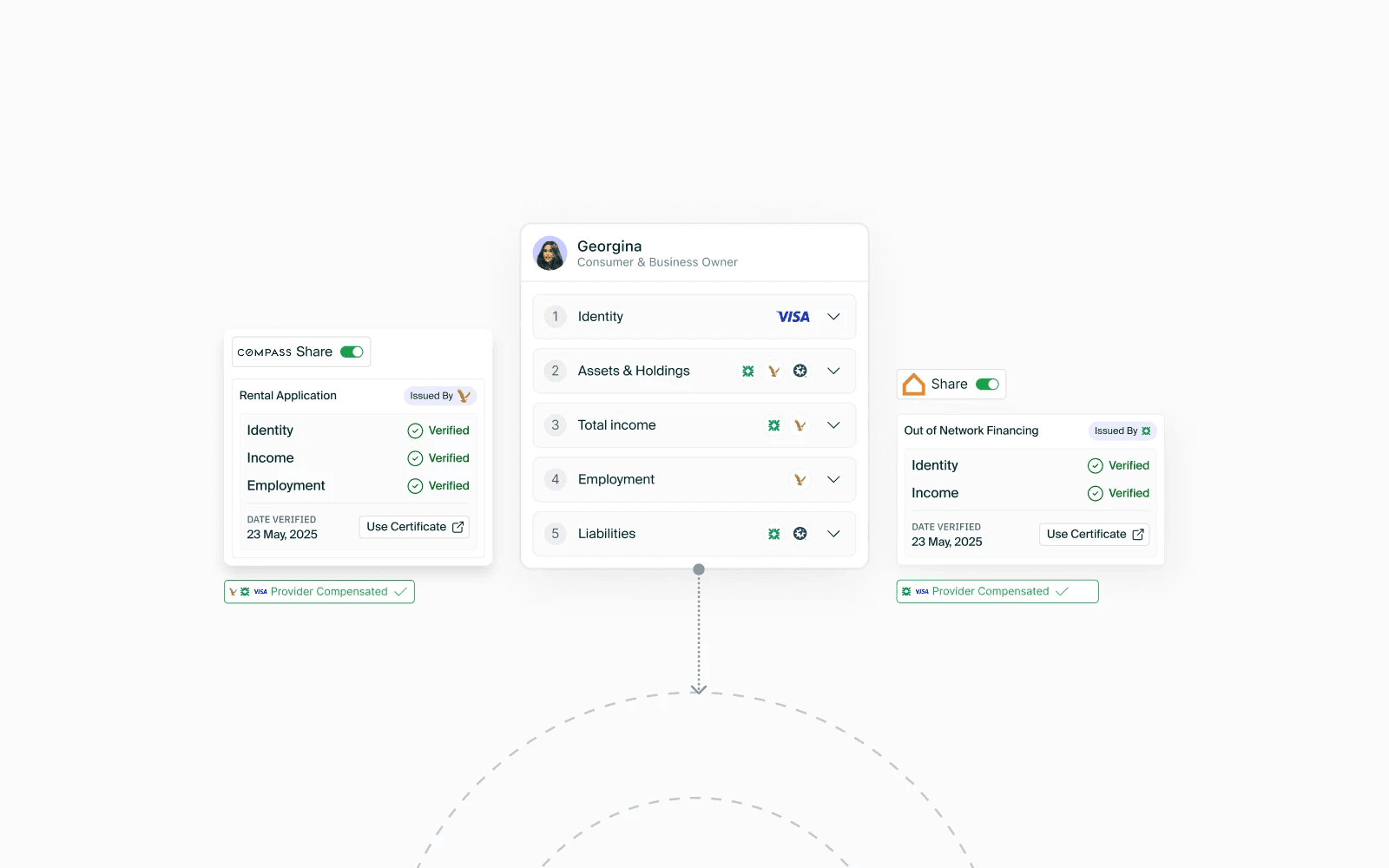

The loudest warning came on architecture. “Transferring data in itself is dangerous for the American consumer,” McCarthy argued. “Lineage must transfer with the data in order for this industry to survive.”

McCarthy continued with a hint into the future. A system where lineage is preserved could open new opportunities for non FDIC insured financial service providers to contribute to an open banking network, because of the way trust could then move with data “Banks create that lineage. Now keep this in mind. Banks create the lineage today. You create it tomorrow.”

A clear consensus emerged: consumers need data that carries its provenance, consent, and recourse throughout the life of the data, not just at the first transfer. Otherwise, each hop resets the trust and destroys the value.

This is the architectural heart of open banking: data must remember where it came from and what compliance work has been done to validate it. Without that, the system will fracture into the same resets that have plagued the past fifteen years.

All three panelists agreed the future needs a new solution, not a preservation of the past. McCarthy cautioned that regulators must resist writing rules to satisfy incumbents: “We don’t want to make sure a single company is not pissed off. We want to write the rule that’s in the best interest of the American consumer.”

The consensus: 1033 should pivot from bank-vs-fintech framing to transaction-specific accountability with consumer ownership, continuous consent, and data lineage at its core. They broadly endorsed a value-based economic model (compensate verifiable value-add, keep raw data near-free), the separation of payments vs. data use cases, and empowering standard-setting bodies to operationalize formats and pricing norms—while avoiding aggregator-supported hoarding.

The next version of 1033 cannot just patch today’s pipes; it must reset the foundation of open banking itself. Anything less is another short-term fix destined to collapse under the same pressures that brought us here.

At SOLO, we encourage the conversation to continue in this direction. Governance should establish clear fiduciary duty for all players. Economics must reward value creation—lineage, compliance, and validation—not rent-seeking. And architecture must ensure data keeps its memory, so consumers aren’t asked to start over every time their information moves. SOLO's network model addresses these aspects directly, detailed in our recent white paper.

SOLO looks forward to continuing to bring together the voices and minds from across the industry to facilitate the conversations needed to make open banking truly resilient for the future. We invite you to join us at our next event, subscribe to the SOLO newsletter below for early access.