BlogOct 20, 2025

Frequently asked questions regarding SOLO's Clearinghouse, a portable trust network that creates "relationship memory"—allowing institutions to recognize your verified history instead of treating you like a new applicant each time.

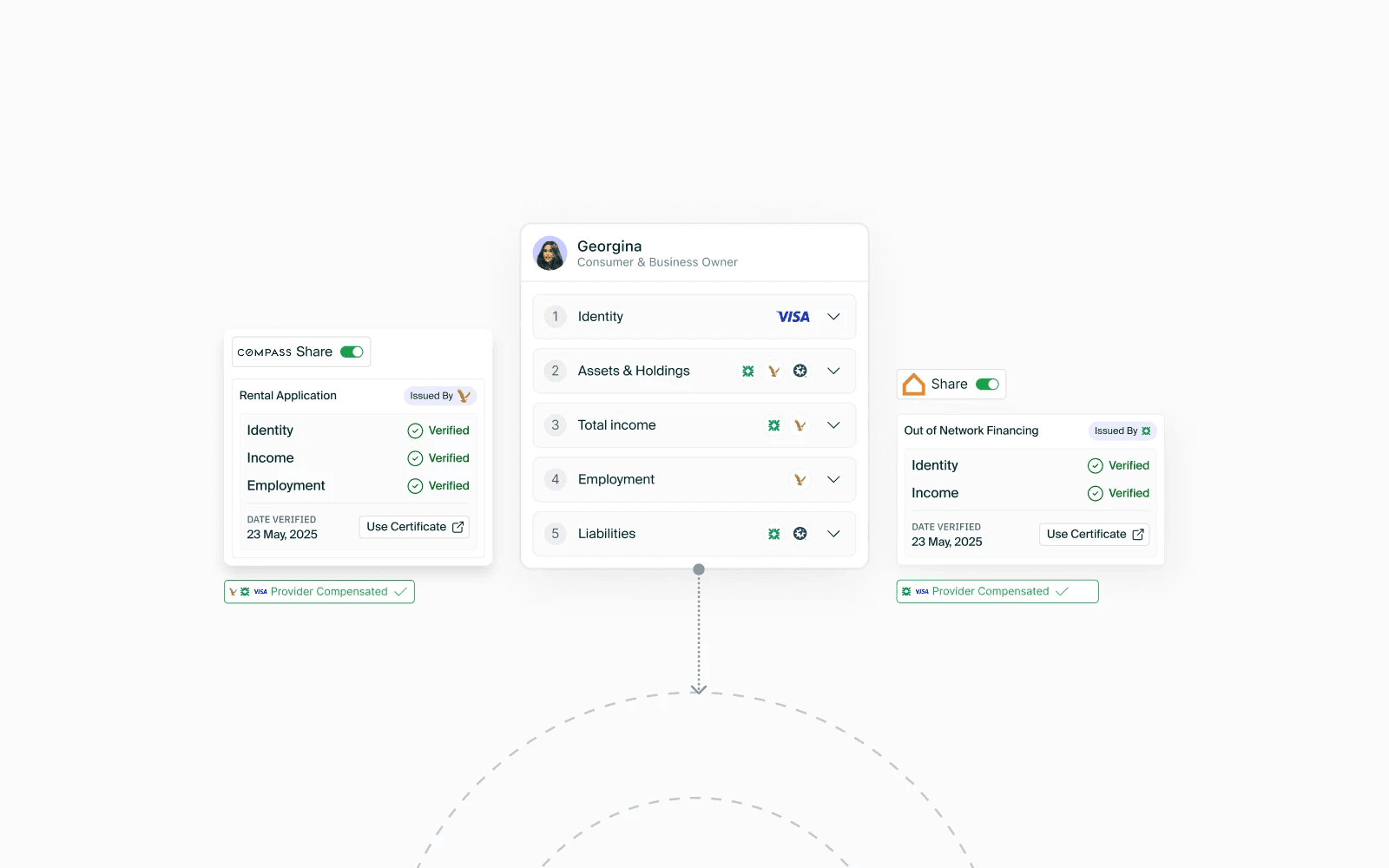

SOLO eliminates the frustration of repeatedly submitting the same documents and explanations to every financial institution. Imagine never having to re-explain why your tax return address differs from your utility bill or re-upload the same files for every application.

The immediate benefit is speed: what once took weeks of back-and-forth can now be completed in minutes. Long-term, this enables a shift from transaction-based to relationship-based banking, where your financial reputation becomes a portable asset under your control.

Our portable trust network creates "relationship memory"—allowing institutions to recognize your verified history instead of treating you like a new applicant each time. Today, banks are incentivized to hoard your data, not help you access services elsewhere. SOLO changes that.

By enabling banks to monetize verified data (with your consent), we align incentives across institutions. Instead of being a gatekeeper, your bank becomes your advocate, helping you succeed across the broader financial network.

The current system is designed for transactions, not trust. Banks pay billions to access and reverify data they already collected. Aggregators scrape incomplete data and resell it, creating more silos. SOLO replaces this reset loop with a shared trust network that compensates the institutions that verify data and gives consumers control.

SOLO is not another aggregator. It is a live, consent-based network governed by banks and built to monetize verified data and eliminate redundancy. With more than 100 institutions already backing the network, SOLO is the only live, scalable alternative to today’s fragmented system.

SOLO follows a bank-led, consortium governance model similar to Visa or Zelle. Member institutions co-develop standards and protocols, with sub-networks to support specific geographies or verticals. There will be more specifics as the network grows and is fully live and transacting.

SOLO reimagines open banking— not as a compliance obligation, but as a value-generating network.

Today’s open banking is one-directional and economically broken: banks are required to provide data via APIs without compensation, while third parties extract value. It’s a regulatory mandate, not a functional ecosystem—leaving banks to bear the cost while aggregators build their businesses on top.

In the SOLO network, verified data is shared only with customer consent, and the data providers are compensated. Data sharing becomes a revenue driver, not a regulatory burden. This aligns incentives across the ecosystem and turns open banking from cost center to opportunity.

SOLO’s network introduces an incentive-aligned economic model where value is created and shared across participants—banks, data providers, and SOLO itself.

Banks and fintechs are paid when their verified data is reused with customer consent. SOLO takes a small facilitation fee, similar to interchange. This turns compliance into a monetized asset across the ecosystem.

The full run down of Clearinghouse economics is available in SOLO's recent white paper.

Yes. Every data request requires explicit, revocable consent. Consumers see who is requesting what and when, and manage permissions through a centralized control panel. SOLO is fully FCRA-compliant and built with privacy at its core. Rather than treating data as an institutional asset, SOLO’s model ensures consumers remain the owners of their information.

Yes — SOLO is fully live and operating at scale. We’ve crossed $1M in ARR and currently support our largest use case — lending—with over $400M in monthly loan volume processed at 98%+ data accuracy. One client eliminated a 9-person data entry team while increasing application throughput 10x.

Fintechs play a dual role in SOLO’s network — as both data consumers and providers. A decade ago, banks held most consumer financial data. Today, fintechs hold the majority, often without contributing back. Many don’t report to credit bureaus, creating blind spots that hurt both banks and consumers.

This imbalance has led to inefficiencies: banks give data away for free, then buy it back at a premium while lacking access to fintech-held records. SOLO corrects this by enabling dynamic, consent-based data exchange where both banks and fintechs are rewarded for verified contributions — always with the consumer in control. The BaaS ecosystem is a prime example, where SOLO helps eliminate redundant verification between banks and their fintech partners, reducing cost and improving compliance.

The regulatory landscape around financial data ownership is in flux. Rule 1033 from the CFPB affirms that customers own their financial data, but recent signals from regulators and industry leaders—like Jamie Dimon’s push to charge for data access—suggest a potential shift away from that interpretation.

SOLO is designed for evolving regulation such as CFPB Section 1033 and is already FCRA-compliant. Its governance, consent framework, and economic structure provide stability even as the rules shift. Consumer control remains central.

The institution that verifies data gets paid when another institution reuses it with customer consent. SOLO’s model encourages verified data sharing, turning compliance costs into shared value.

Learn more about the Clearinghouse incentive structure in the white paper.

SOLO’s platform is built on a four-layer architecture designed to fix the foundational flaws in financial data infrastructure—eliminating fragmentation, manual effort, and one-time interactions.

SOLO’s four-layer architecture includes: Memory (auditable data storage), Resolution (AI-powered verification), Network (secure, compensated sharing), and Activation (actionable insights). It works across formats and institution types, making trust scalable.

Learn more about how the Clearinghouse works in the white paper.

SOLO is currently accepting founding partners to pioneer the Clearinghouse alongside confirmed early adopters. To learn more, contact the SOLO team.