BlogOct 20, 2025

And SOLO's Playbook for Banks

On one of our diligence calls before BankTech Ventures invested in SOLO, Carey Ransom said something that stuck with me (I still have the notes):

“There are three types of small businesses." He went on to break it down:

When we started automating small business underwriting, we (incorrectly -- several years ago) thought most businesses fit into bucket #1 — ambitious, growth-driven. The reality? Most borrowers are in bucket #2 — small by choice.

And that changes everything.

Companies like Ampla, ClearCo, Pipe, Stenn (the list goes on) tried to solve this problem but built products based on their own biases. They were “small by age” high-growth startups building for businesses just like themselves — tech-savvy, growth-obsessed, and operationally sophisticated.

So, what did they build?

But here’s the problem: Most small businesses don’t run like venture-backed startups. They’re not living inside SaaS dashboards or keeping books updated in real-time.

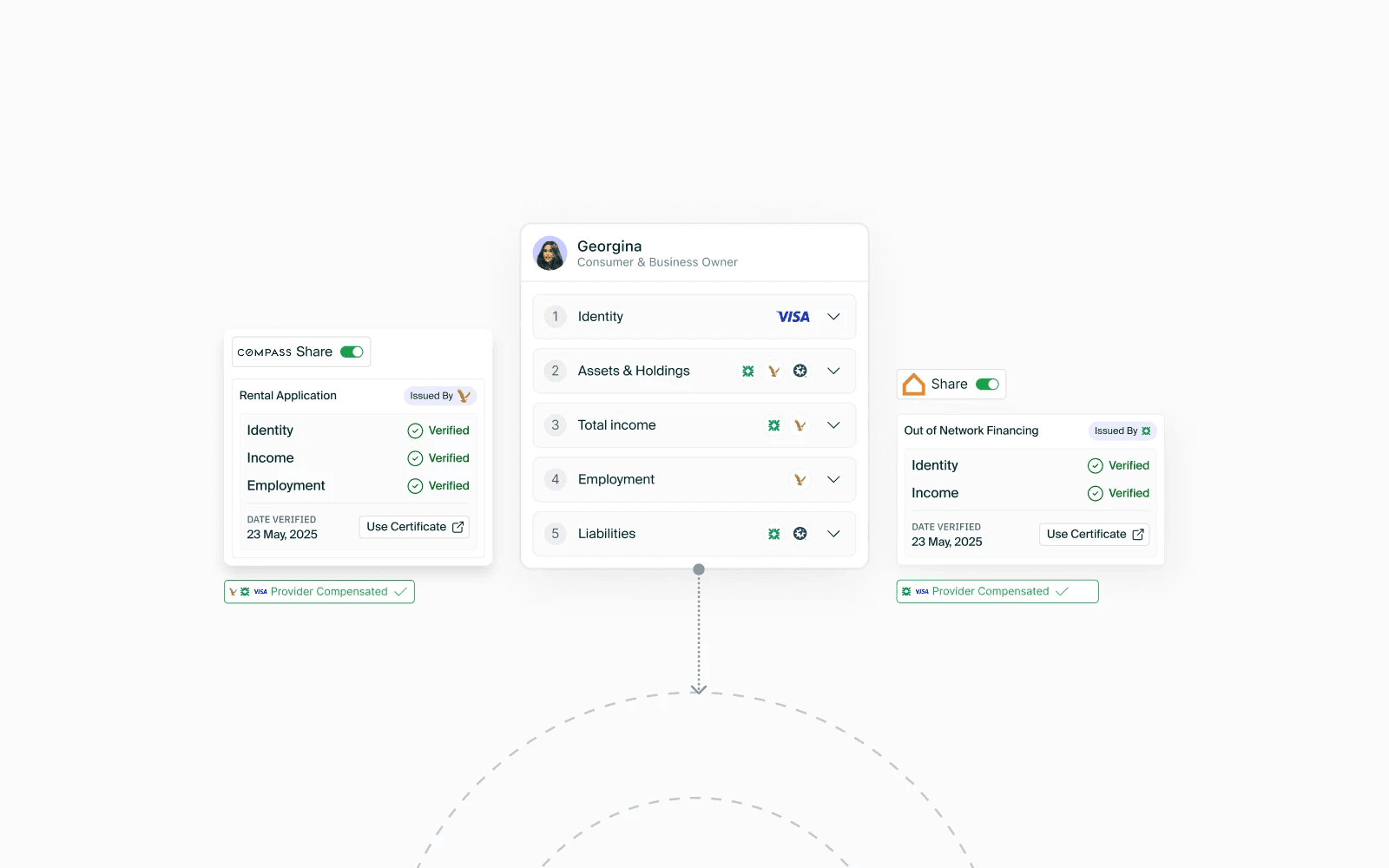

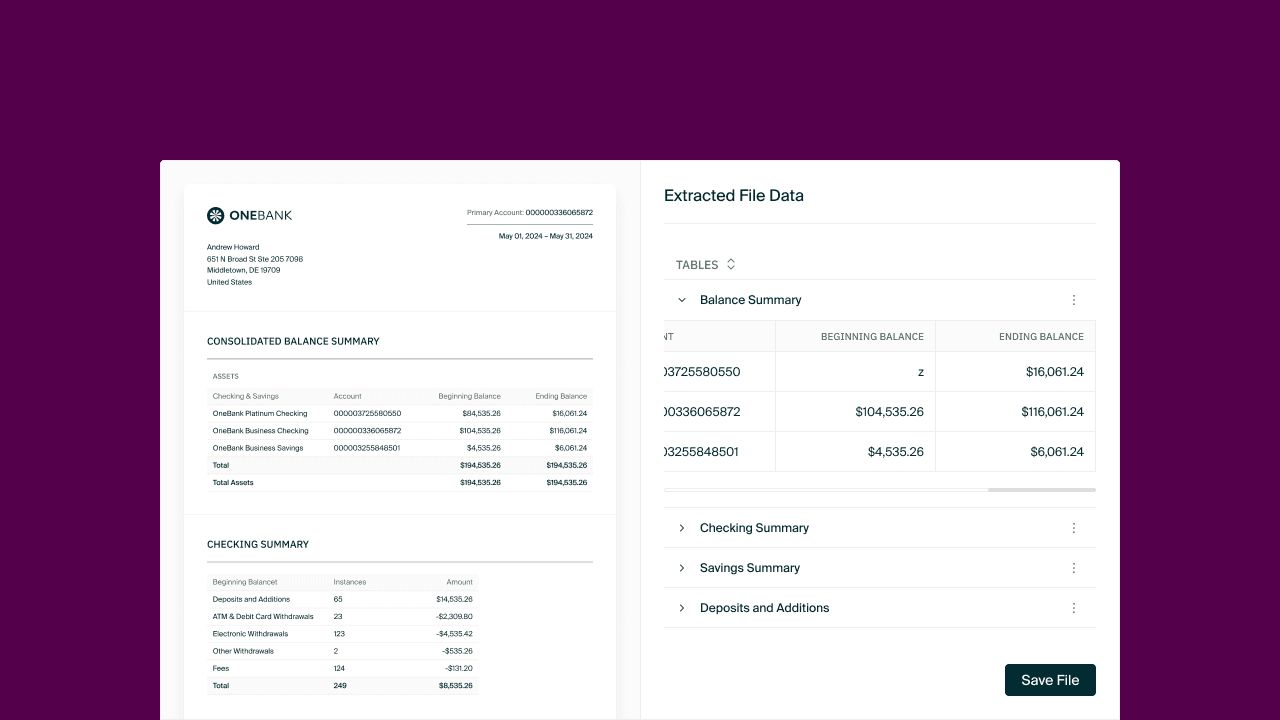

So, these solutions ended up being just that — pretty interfaces. If your onboarding looks good and connects accounts but doesn’t generate financials for the borrower during onboarding, or feed into the back-end systems—to run spreads, calculate debt service coverage ratios, assess credit quality — then it’s just a glorified (and super expensive) google form.

You’re not solving the problem. You’re just making it look better.

It’s a data problem, and the real challenge isn’t just missing paperwork — it’s re-engineering the data to fit your lens because of the variance in how it’s provided.

One of our clients said something recently that stuck with me: “The enemy of automation is variance.”

And small businesses are full of it:

This variance is why underwriting small business loans is so hard. It’s not about data quantity—it’s about data quality and standardization.

We realized the problem isn’t just about collecting data—it’s about transforming it into something lenders can actually use.

It’s about:

Because at the end of the day, it’s not just about collecting data. It’s about making that data work—for both the lender and the borrower.