BlogJul 29, 2026

How Rob Frohwein, Co-Founder of Kabbage, mastered high conversion financing and exponential origination rates.

Requesting access to an account. Will it ruin application rates or power an 85% conversion rate like Kabbage? Learn how to...

1. Incentivize borrowers to opt into data sharing.

2. Leverage connections to increase customer value.

3. Maintain connections to shape product innovation.

From the Co-founder and CEO with a proven record of:

→ 85% application conversion rates

→ $9 billion in capital deployed

→ 240,000 SMBs served

Watch the master class on building high conversion loan experiences with account integrations. Led by SOLO advisor and the Co-Founder/CEO of Kabbage, Rob Frohwein:

Ready to launch a financing application with account integrations? Try a custom Template.

“This isn’t just a competitive edge—it’s the future of lending. Borrowers are increasingly expecting seamless, data-driven interactions, and it’s no longer a matter of if but when all lenders will need to adopt these systems.”

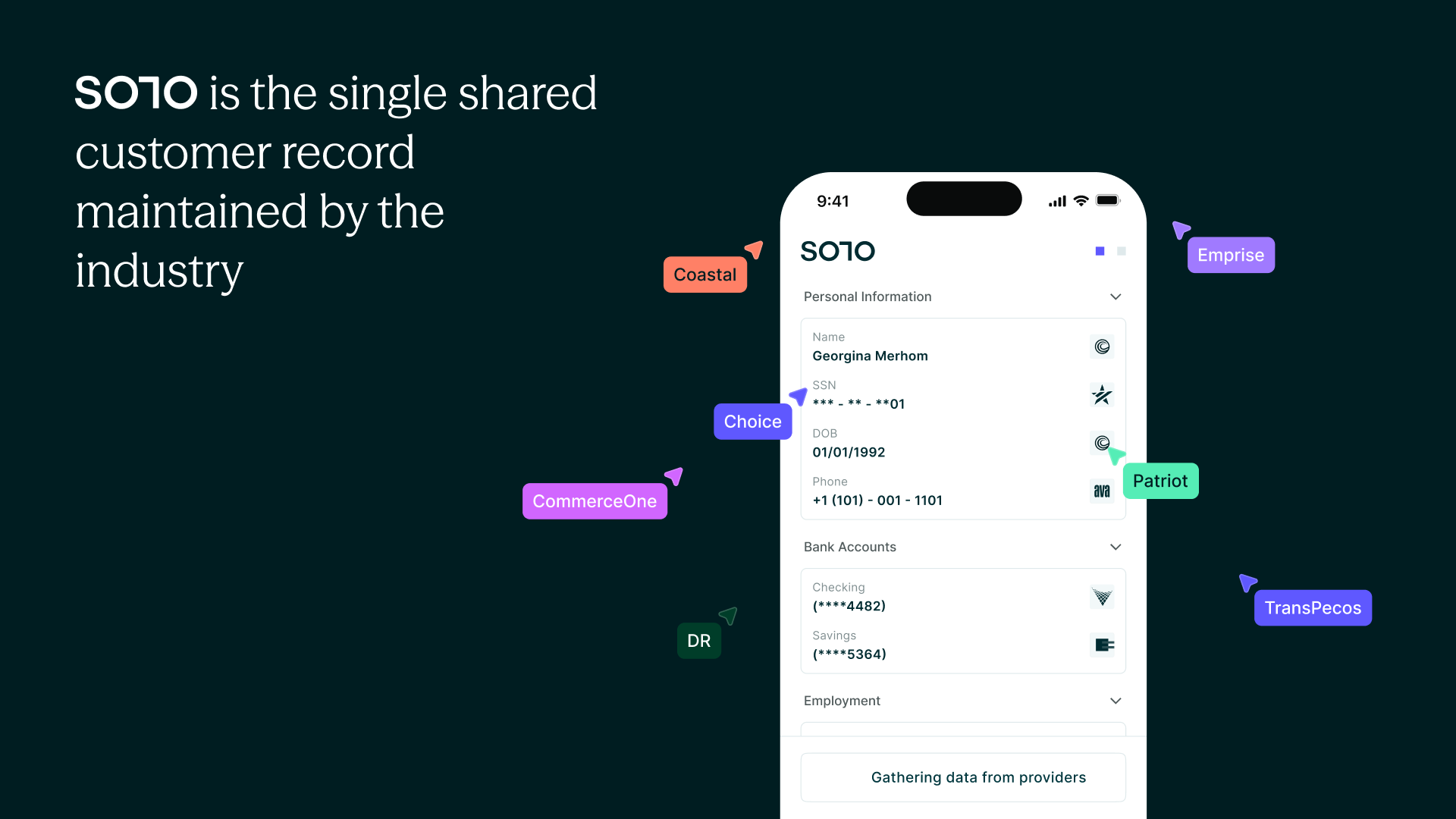

A good digital experience for borrower applications isn't just about speed. It’s about leveraging new tech an to redefine relationship banking for the modern world.

Data integrations are at the heart of this transformation. They enable lenders to collect, process, and analyze borrower information seamlessly, reducing manual steps and creating a more transparent, efficient, and borrower-friendly application process.

By eliminating the clunky paperwork and asking borrowers to connect accounts, lenders can simplify workflows from first introduction while fostering trust and satisfaction over time with proactive product matching that fits their real time financials.

For borrowers, this means reduced friction, personalized offers, and clearer pathways to financial products. In this way integrations unlock the ability to power a true ongoing partnership with customers. Turning underwriting from a static, high cost, one-time instance into a continuous service to scale relationships through continuous underwriting.

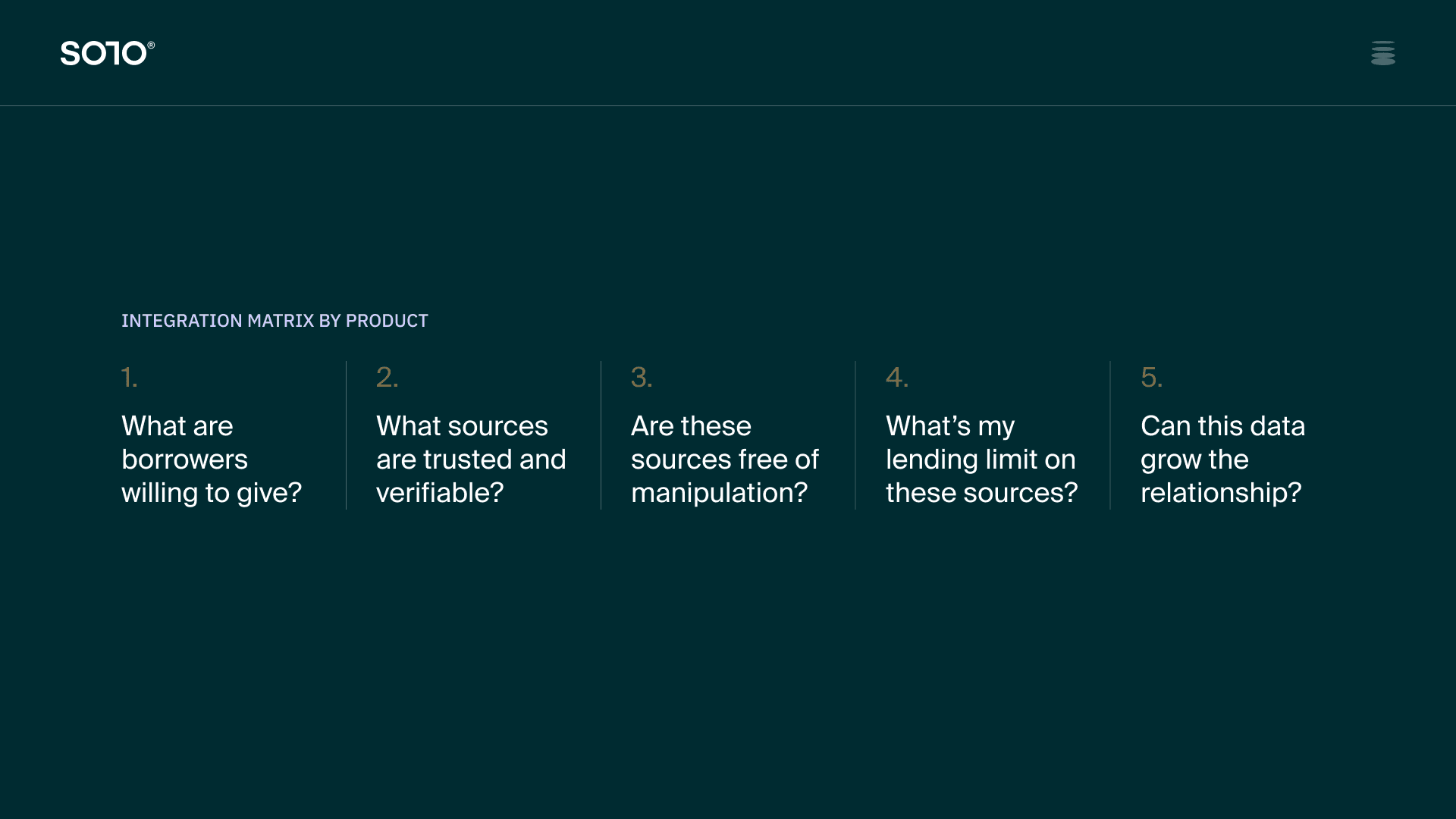

Selecting the right integrations is critical to the success of a financing application.

The key is aligning integrations with underwriting needs and borrower incentives. Kabbage initially connected to platforms like eBay to gather transaction data, paving the way for personalized credit decisions.

Now, lenders may leverage any number of data sources or combinations of integrations to map real time, verified data to an automated underwriting process flow.

A simple framework for choosing integrations to power automated underwriting:

The Solo Application Builder empowers lenders to create dynamic, no-code financing applications tailored to their needs. The process begins by understanding the current underwriting workflow and mapping out data sources.

Ready to test financing applications with account integrations? Connect with the SOLO Implementations team for a customizable template for your institution.