BlogJul 29, 2026

Solutions

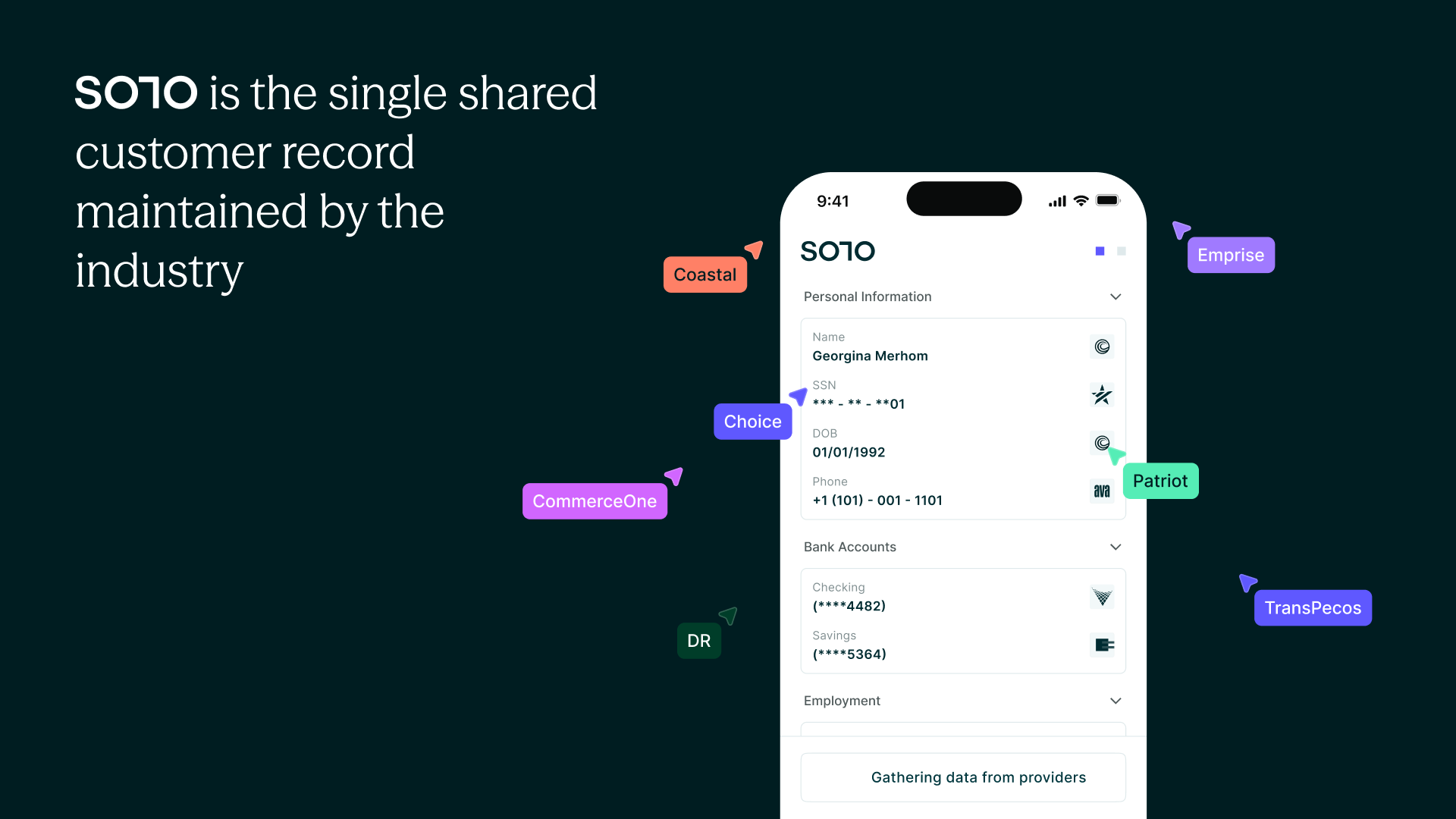

An Action Plan for Transforming Customer Data Collection from a Costly Liability to a Revenue-Generating Asset.

This article is excerpted from The Banker's Roadmap to Digital Lending. Download the full White Paper below.

Community banking is in a deciding moment. How, and should, community institutions introduce a digital lending platform?

“We have to evolve. And there's certainly an acknowledgment at the board level and a senior leadership level about the need to continue to invest in creative ways to serve the customer; especially through digital channels.” - Community Banker

According to the FDIC’s Small Business Lending Survey, digital lending is a priority for banking leaders, specifically for retaining market share and profitability.

Half of FDIC surveyed banks were already using or considering FinTech in their small business lending process to automate underwriting processes. However,

Banks of all sizes have already found ways to streamline simpler credit models with straightforward underwriting processes using technology. However, automating more complex underwriting processes, like those for small business lending, go largely unsolved.

These underwriting flows remains a highly manual, high touch experience despite the desire to evolve with new technology.

“When we’re talking about paper back and forth, it’s a nightmare.” - Community Banker

C-Suite leaders and their direct reports shared that, although digital transformation is a priority for leadership, launching a digital lending platform remains a puzzle fragmented by the challenges faced with complex siloed tech stacks, internal friction, compromised customer experience, concerns of accuracy matching with efficiency, and of course: profitability.

This is most clearly illustrated in relationship based transactions.

Top of mind for the bankers SOLO surveyed: finding a solution to retain the uniquely competitive qualities that define community banks from larger institutions while developing the ability to compete with larger and nonbank lenders in the digital landscape.

Small to midsize banks typically are seen as having greater advantages for cultivating relationships that power the collection of what the FDIC coins as “soft information”.

Approvals incorporating both hard and soft data determine credit use a wider scope of supplementary financial and personal information in addition to the bureau determined credit score.

The leaders we spoke to were in agreement that this is a competitive advantage community bankers possess, rooted in their unique sense of community validated trust that enables "soft" data collection. It is often a draw for borrowers seeking a certain level of customer service and experience.

Historically, the draw of relationship based banking has enabled organic growth at an institution while facilitating more individualized credit decisioning. Customers feel like people, not a number in an algorithm.

However, community banks share struggles to build robust pipelines for their legacy products. The focus on relationship-based transactions is still a defining advantage for community and regional lenders, yet it’s also now one of the most significant roadblocks to full adoption of digital lending processes.

What’s the liability of adopting technology to replace legacy processes of credit decisioning?

Is there more risk in simply maintaining the status quo?

The C-Suite bankers SOLO surveyed reveal the sentiments guiding community bank strategy today, including the concerns, potential, and readiness factor of banks for digital lending solutions.

Their responses depicted a keen awareness of the need for innovation, rooted in a practical reality of facing the challenges to do so, primarily in:

| Efficiency. | Experience. | Expense. (or, Profitability).

66% of respondents believe in their institution’s ability to adapt to the financial needs of SMB’s with varying business models, which manifested in 1 main way:

The bank possesses a cultural and process-driven commitment to keeping an open mind and thoughtfully evaluating revenue potential for new segments.

“We have to evolve. And there's certainly an acknowledgment at the board level and a senior leadership level about the need to continue to invest in creative ways to serve the customer; especially through digital channels.”

One theme that respondents shared when it comes to adapting to varying business models is that it heavily depends on two things:

1.) the customer’s revenue band

2.) the bank’s ability to scale that solution for other clients and segments.

Banks are likely prioritizing revenue potential over all other factors.

Of the ~30% of bankers who did reveal a struggle to adapt to the financial needs of SMB’s with varying business models, the biggest roadblock to progress was internal buy in. The problem manifested in 1 main way: the bank possesses an old school mentality that is resistant to change and instead wants to focus on existing segments they’re more familiar with.

“If we have to come up with a custom solution for somebody that usually takes a lot of time and effort and the bank avoids that as much as possible.”

One banker stated that it takes a lot of time for the bank to come back with new or custom solutions, and that this impacts their ability to grow revenue and acquire new clients.

Another, that customers often threaten to leave, which is demoralizing for the lending teams and damaging for the bank’s culture when they lack support for outside-the-box ideas.

(defined as time from interest to funding/completion).

Friction developed when banks attempted to deliver products efficiently, manifesting in 2 main ways:

The resulting burden is shared between bank and customer.

84% of respondents felt the impact of delayed approvals, which manifested in 3 main ways:

Delays at the data collection stage are a primary paint point shared by leaders.

“As a business, you’re putting the customer in a very legacy and manual experience. They will go find a better bank with a digital capability to interact with.”

Another banker articulated the challenge in verifying and trusting the integrity of customer financials, even if the customer is willing to engage in a paper-based process.

“Typically small businesses are busy and not focused on their financial well-being in the way that I think the financial services industry expects them to be.”

“If people aren’t staying on top of their responsibilities for data collection, it’s taking time away that they need to be spending on other responsibilities. I become concerned about the level of time that servicing takes our team.”

Our C-Suite also shared that their banks endure a major reputational risk and an inability to stay competitive when they’re not able to turn product requests around quickly.

Of the respondents who felt this problem was impacting them in a meaningful way, 63% of bankers either had attempted a digital solution or are actively seeking one.

The problem manifested in 1 main way: the surveyed banks lack the technical ability to access 1st-party data and relying solely on self-reported financial data from customers to identify expansion opportunities.

It’s interesting to note that all bankers who reported inability to approve borrowers in 24 hours also noted the inability to leverage data for expansion, suggesting a link exists between initial data collection processes and data’s role in customer lifecycle management.

Bankers noted that while a solution has yet to come to fruition, data collection and management for increasing customer LTV is a topic of high interest, clearly reiterating the value it could create for community banks and lenders.

Several bankers noted that a strategy or attempt has been made, although with underwhelming or inconclusive results:

“We need to have a more platform based approach to data collection and the right way to do that is what we're currently trying to figure out. So currently we have email based communication with reminders.”

“We're trying to make sure our onboarding is 24 hours as opposed to three weeks. Every day we're getting closer and closer to that. We want independent verification of customers’ data, but I think we're trying to build those connections initially through the onboarding process.”

“If we’re looking at the lower end of the market, we’re a lot more reliant on bankers and sales folks to have those data conversations. At the upper end, I do think we’re more data driven to make sure we can come up with the right solution packages.”

Examining the pain points of bankers, SOLO developed a technology and philosophy around digital lending to address the needs of the industry with the expertise of our team’s data science foundations.

We believe a true digital lending platform begins with establishing a system to prevent inaccuracies in automated decisions by shifting focus back to the very beginning of the lending process.

Algorithmically determined decisions are only as reliable as the inputs used within them. The finer points of the Digital Lending roadmap stem from our core philosophy of data collection and governance within digital lending.

Subscribe Here for Full Access to The Digital Lending Roadmap.