BlogJul 29, 2026

Solutions

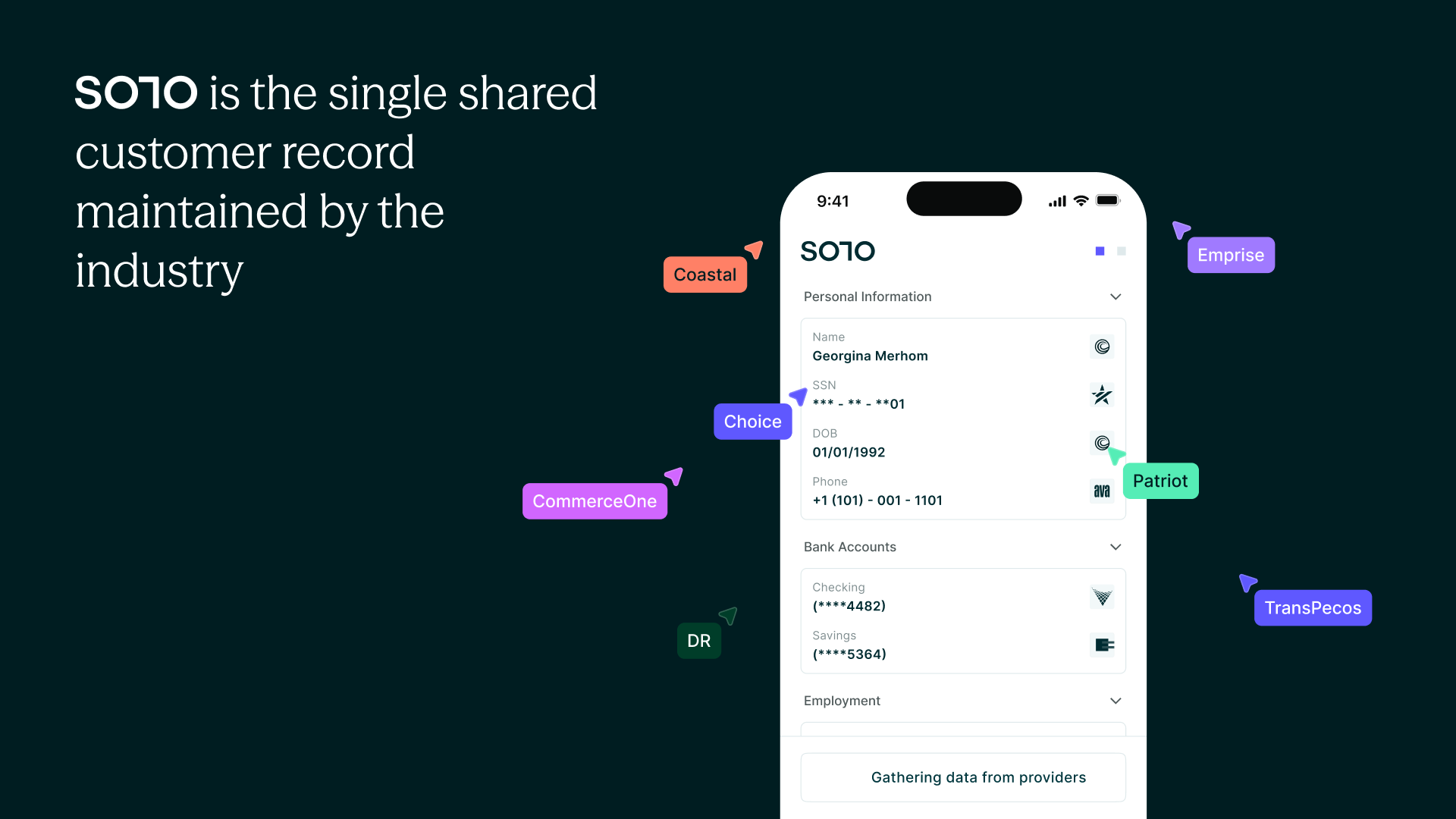

Customer-permissioned data sharing makes credit more dynamic, transparent and accessible.

BankTech Ventures, a strategic investment fund and ecosystem serving community banks and bank technology entrepreneurs, has invested in SOLO, a collaborative data collection platform that transforms underwriting from an expensive, one-time, opaque process into an ongoing, proactive, and transparent system that identifies the path to any financial product or outcome, fostering open dialogue and collaboration between banks and customers. Developed alongside BankTech Venture’s network of community banks, SOLO’s platform enables secure, streamlined data collection and activation, empowering banks to make more efficient and proactive underwriting decisions.

SOLO addresses the key challenges facing financial institutions with traditional credit reporting and assessment, including maintaining data accuracy, complying with evolving standards and managing operational costs. Designed specifically for banks, the platform streamlines financing timelines with frictionless applications, data collection powered by consumer permissioned account integrations, on-demand decisioning, continuous 360-degree underwriting capabilities and proactive product matching.

By creating a "record of truth" for each consumer, SOLO allows users to own their credit data, while banks query the data they need in real time, optimizing both efficiency and customer experience. The result is a shared language of credit, eliminating the back and forth between customer and banker to put all parties on the same page at first introduction.

“SOLO’s unique ability to address the present needs of banks and their customers, while still building for the future, is what sets them apart,” said Carey Ransom, Managing Director at BankTech Ventures. “This investment signals a shift in how banks become more efficient and scalable in their lending, particularly for banks adapting to new standards of data governance within digital lending.”

“Our mission is to foster collaboration and trust across the financial ecosystem, turning data-sharing and data collection from a tedious task into a reusable asset that establishes instant credibility to open doors.” said Georgina Merhom, founder of SOLO.

The current underwriting stack provides a static, one-time snapshot of a consumer’s or small business’s creditworthiness, costing banks $100–$400 per underwriting event. Underwriters must verify and standardize data from multiple sources across several open tabs, making the process both expensive for banks and frustrating for consumers. This approach also fails to clearly outline the steps a consumer or bank can take to achieve a financial goal or product qualification.

With SOLO’s 360-degree, consumer-permissioned data collection, banks gain year-round visibility into a customer’s creditworthiness. This enables ongoing opportunities to match customers with products, providing a clear and collaborative path to qualification—without requiring multiple application rounds.

The SOLO platform is currently undergoing FCRA compliance certification, with plans to operate as a Certified Reporting Agency by early 2025. By offering a “collaborative credit bureau” model, SOLO aligns with the Consumer Financial Protection Bureau’s (CFPB) mission to advance open banking with the newly published 1033 rule. SOLO transforms credit scoring from static to a dynamic, context-aware evaluation system, enabling users to engage various stakeholders in building a more comprehensive credit profile.

SOLO’s aim is to foster collaboration not just in scoring models, but across the financial ecosystem, democratizing data sharing, reporting, and trust-building. This approach empowers financial providers, consumers, third-party vendors, and the broader community to co-create a more transparent, inclusive, and accountable financial landscape for the mutual benefit of all the stakeholders in the equation.

“Banks face a critical dilemma: maintain manual processes and sustain higher operating expenses, or risk being forced to charge higher interest rates and loan spreads. This cost burden inadvertently triggers adverse credit selection, as top-tier clients naturally migrate to more competitive offerings, often with one of a few dominant banking players,” Carson Lappetito, President of Sunwest Bank, “As community banks, our goal should transcend mere cost-cutting. The true objective is to strategically narrow loan spreads, systematically attract the right clients, and construct a sustainable, long-term profitability model. That’s how we achieve a more competitive model for business and for the customers we serve.”

Drawing inspiration from the traditional community banking model, SOLO scales values of personal relationships and local knowledge through advanced technology. SOLO’s platform preserves the core principles of trust and social accountability that define community banking.

“The way we’re building the credit bureau is fundamentally collaborative,” says SOLO’s founder, Georgina Merhom. “We’re scaling the trust-based ethos of community banking, making it viable, profitable, and scalable across the credit ecosystem.”

SOLO is the collaborative credit bureau transforming how credit data is collected and activated. Developed alongside a network of community banks, the SOLO data ingestion platform syncs data from various sources, giving lenders control over calculations and interpretations to shift the burden of verified financials off the consumer while mitigating the risks of unreliable self-reported information, fostering accuracy and trust in decision-making.

BankTech Ventures identifies and invests in leading bank technology companies and is deeply entrenched in community banking to ensure its companies work effectively and efficiently with banks to deliver maximum value and impact. BankTech’s unparalleled ecosystem is designed to deliver compelling innovation with community banks at the center of it all - bringing together bankers, industry organizations and tech founders to work collaboratively to accelerate innovation in banking.