Index

CATEGORY

Best Practices

Use Cases: AI for Credit Underwriting

Use Cases for Applying AI to Automate Documents and Processes in Credit Underwriting for banks, lenders, and credit unions.

Feb 13, 2025

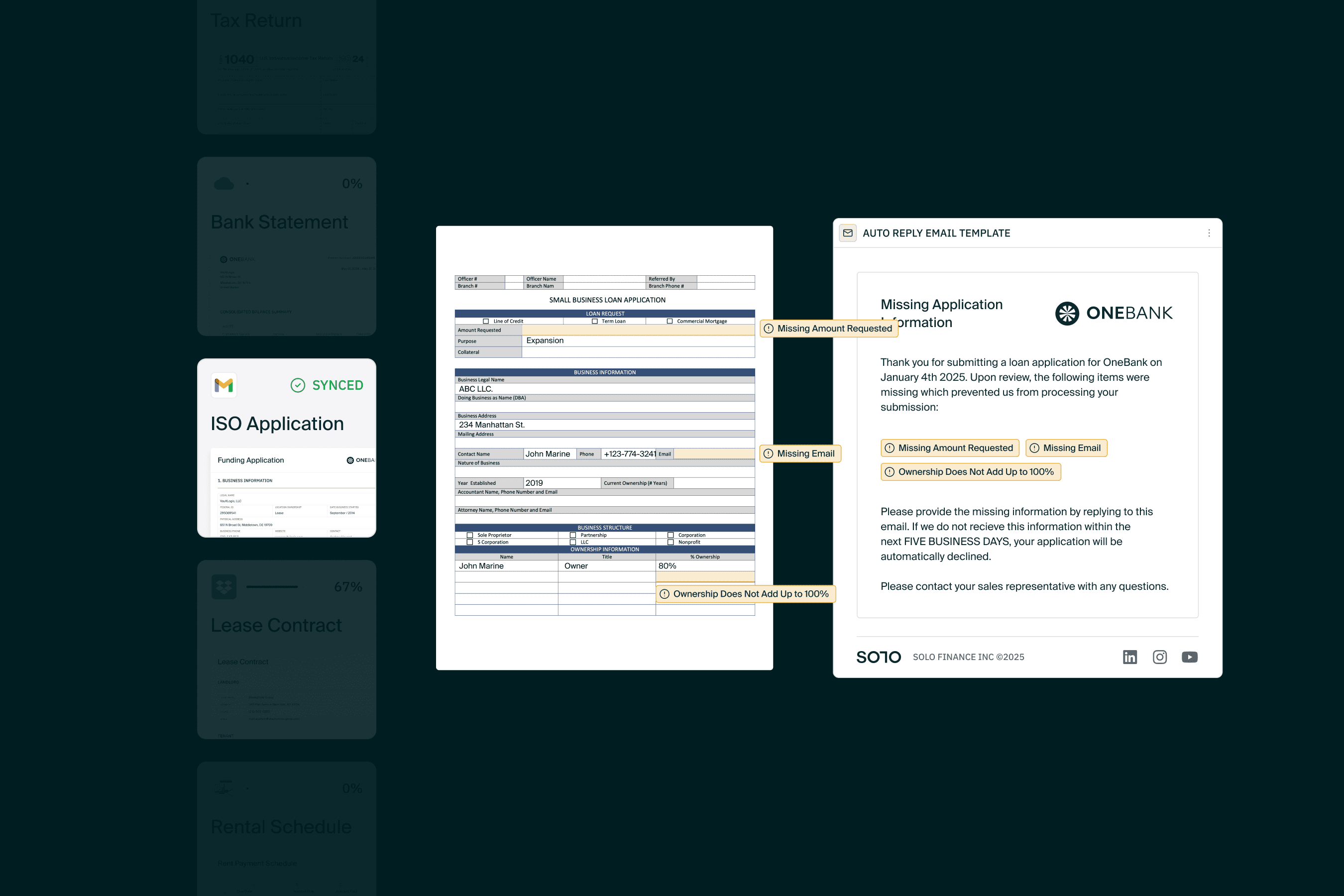

1. Flag Missing or Incorrect Fields in Loan Application Documents and Automatically Follow Up for Underwriters

Every month, underwriters lose hours chasing missing information, copy-pasting across tabs, and stitching together fragmented systems.

Not making judgment calls.

Not asking sharper questions.

Just moving pieces around.

The Flag & Follow Template is a plug and play document automation for lenders to automate the admin of document processing.

Ingest documents from a shared Sales inbox, flag and follow up on missing fields, re-process data from email replies, and structure complete data into an actionable report. Go from incomplete PDFs to CRM ready deals with 0 manual re-keying of information, without pulling underwriters away from the work that actually demands their judgment.

2. Build High Conversion Borrower Applications

Use automation to strengthen digital loan origination by improving borrower experience at first application with frictionless applications that sync data from a seamless front end UX into workflows, rules, and across systems.

A high conversion application should leverage automation to make a credit application:

Simple for the borrower to provide all their information and view all their options, almost immediately.

Seamless for bankers to analyze for a decision and action across their existing platforms and systems.

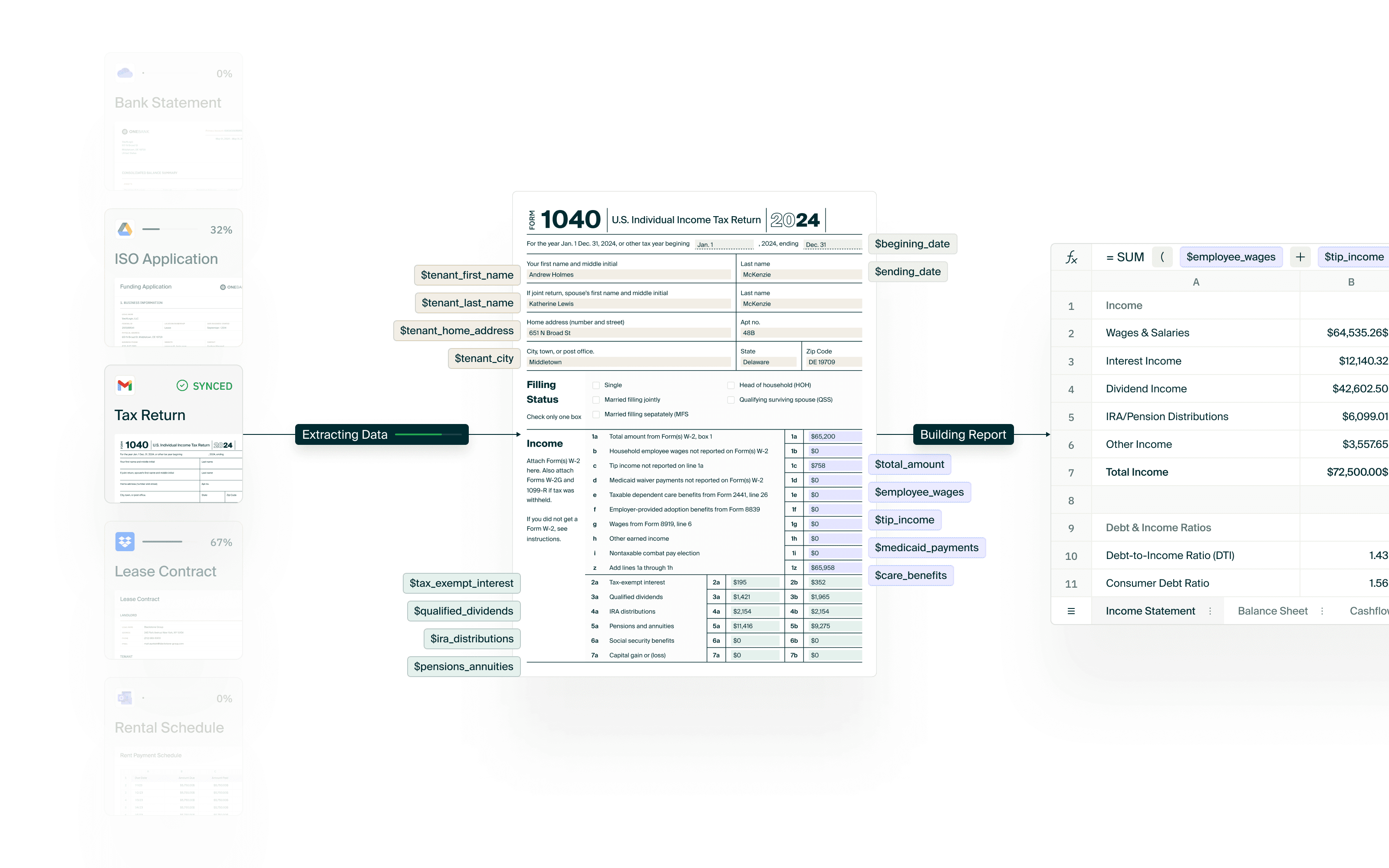

3. Automate Financial Statement Creation for Borrower Paperwork

Gathering, verifying, and spreading borrower financials in a credit workbook is a complex process and is the root of most friction within a credit application.

SOLO's front facing borrower onboarding portal was developed to eliminate friction for borrowers and the bankers underwriting their loans by generating financials for borrowers, automatically synced to the lender's automated spread.

01 PULL autofills an application and automates financials statements according to the lender's accounting methods from a borrower's raw data, including:

Balance Sheets

Income Statements (profit and loss statements)

Financial Projections

Cash Flow Statements

On demand, from just their connected accounts and uploaded documents. Learn how we're powering the shift from self reported financial statements to autonomously generated financials.

4. Turn PDFs Into Portable Data Sources for Automated Underwriting Workflows to KYC in Minutes

Use AI to read financial documents like bank statements and financial projections as well as unstructured data in the form of PDFs or Rich-Text Files submitted as part of a credit application.

SOLO's intelligent document processing for Credit and Underwriting reads any document or group of documents, and extracts every data point needed for a verification. So underwriters and borrowers can upload anything, and pull borrower information directly into the file format, workflows, and systems needed for credit teams to scale underwriting efficiency.

Demo Document Intelligence from SOLO.

5. Apply Custom Credit Scoring Frameworks per Product

A major opportunity unlocked by AI for credit underwriting is the new ability to create systems that make context aware credit decisions viable at scale.

A context aware credit decision processes significantly more data points, run through tailored scoring frameworks that consider more nuances of creditworthiness in addition to a standard credit score. Automation can give lenders the power they need to fully consider borrower creditworthiness in every context, for every product, with a unique scoring framework for each instance.

SOLO supports context aware credit scoring by creating a record of truth for each individual and business, which lenders can continuously view through their lens of credit for every product in the portfolio. Leverage automation to transform underwriting from a high cost, one time event into a continuous partnership.

6. Proactively Underwrite and Match New Product Fits by Automating Calculations from Real Time Data

Once automation is properly applied at the beginnings of the underwriting process for credit document collection, standardization, and activation data can be leveraged to unlock opportunities over and over again.

Leverage continuous data integrations and seamless document intelligence to stay synced to borrower financials in real time at all times, and proactively match to new products as needs and eligibility change.

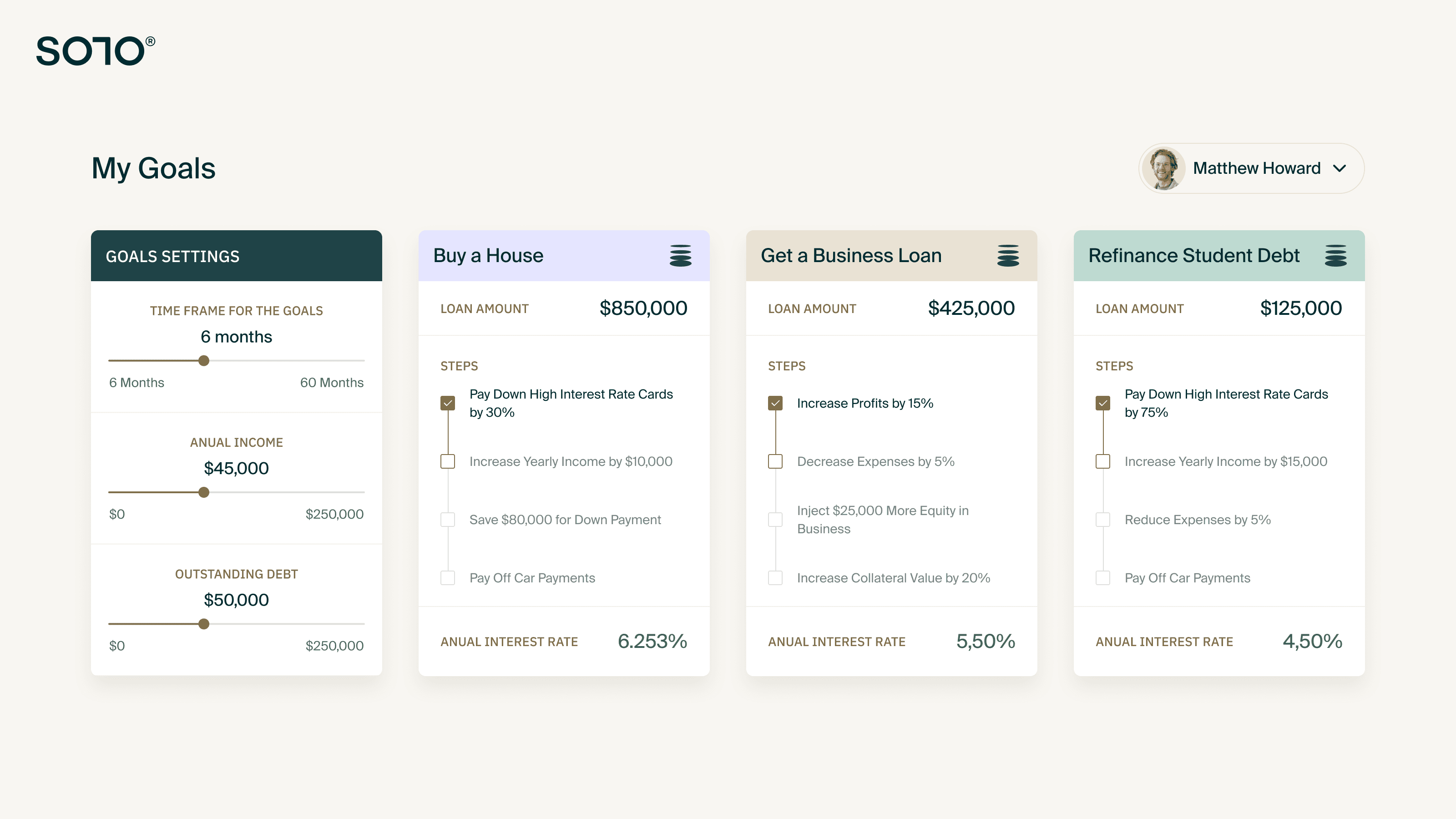

7. Generate Custom Roadmaps for Customers to Track Their Progress

When digital account opening is connected to an automated underwriting spread, banks can continuously provide borrowers visibility into their next steps for eligibility at their institution. Create dashboard that stay up to date with borrower data and give actionable next steps, additional options, and support to borrowers growing their relationship at your bank.

Automation in underwriting processes isn't just for speeding up decisions. Automation is a bank's most valuable tool for doing what they do best: scaling relationships with best in class service. That starts with an efficient and repeatable underwriting automation, so financing applications aren't just a one time yes or no decision but a true partnership.