BlogJul 29, 2026

By the founder and CEO of SOLO, an embedded platform that provides capital markets with real-time access to autonomously reported, standardized and verified financial statements of SMBs.

Imagine a world where "AI VC", “AI Bank” or "AI Financing" entities could deploy capital independently, without the need for investment committees, bank officers, or credit analysts.

What would it take to make this a reality, harnessing AI to deploy capital to businesses with no human intervention?

While we can't claim to have all the answers, we believe automated decisioning is a viable reality, but only if we revisit the most basic principles of generative AI models.

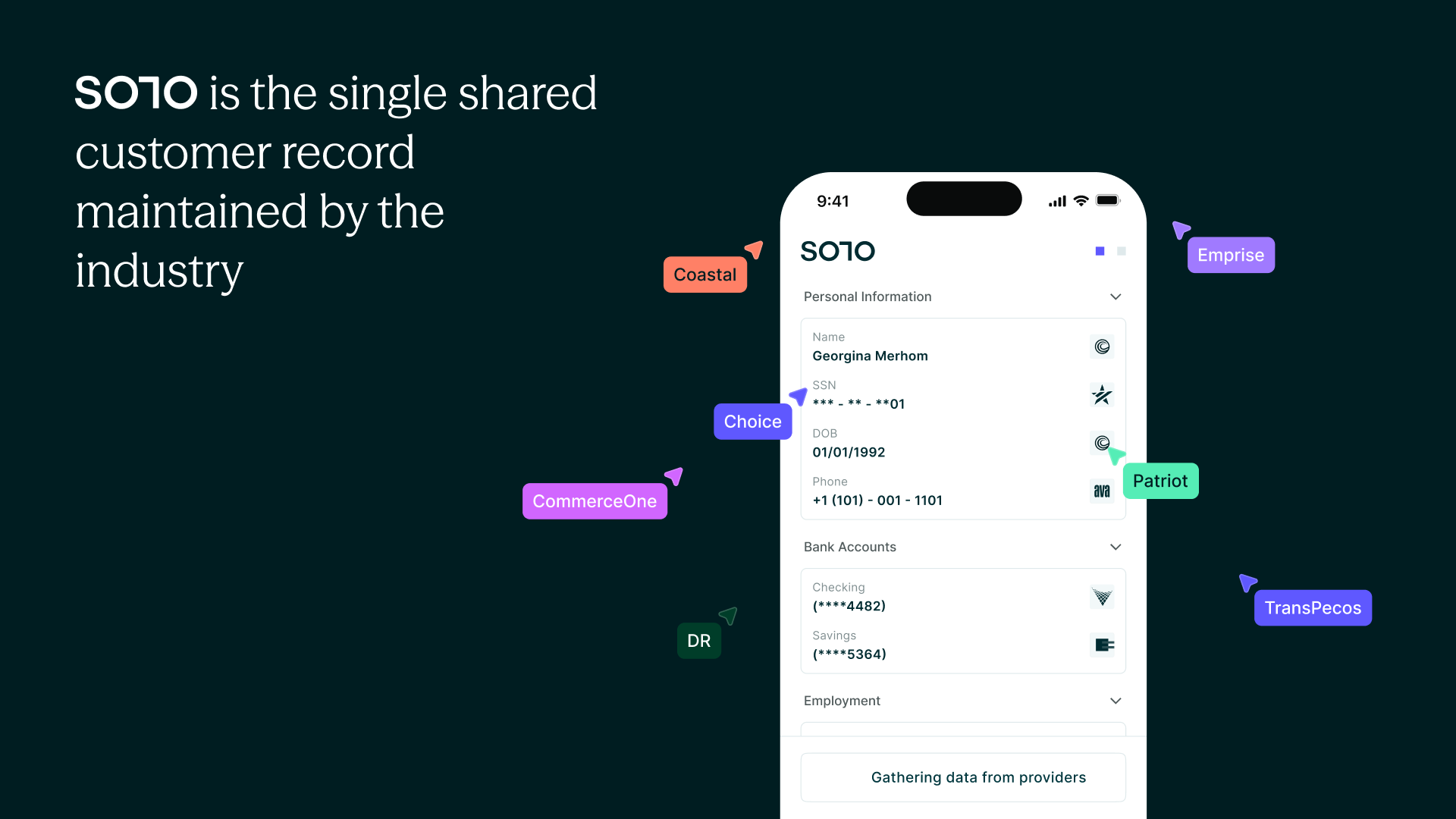

The first step to building a true AI powered Bank would be to replace self-reporting with autonomous reporting, to have operating systems that autonomously report on behalf of SMBs, to be able to standardize, verify and get a “real pulse” on every business.

While my biography says I’m the founder of SOLO, a fintech startup, my point of view is inherently shaped by my earlier career as a data scientist.

I was first introduced to the world of automated decisioning working on an algorithm that employed network analysis and algorithmic quantum computing to identify the finance manager within a decentralized terrorist network.

In today's era of accessible information, a prevalent misconception in the field of decisioning is the belief that more data, and more insights, equates to more accurate decision-making algorithms.

My journey in cybersecurity unveiled a fundamental truth conflicting with popular perception of AI—accessing data is merely the tip of the iceberg.

I’ve witnessed security algorithms highlight the fault in this argument, delivering up to a hundred thousand false positives for every real threat detected.

A trusted decision is not derived from more data, it is always contingent on the quality, source, and integrity of the data.

In order for the excitement for automated decisioning to be merited, we must revisit the very foundations of the model to do so. We must start back at the beginning.

There's a conspicuous and at times overly inflated narrative surrounding generative AI, still positioned as the zenith of progress in finance.

The assumption is often that generative AI brings lenders value in its quantitative processing power: the more data points the model processes faster, the more assured we can be in its output even if we’re not fully able to rely on its decision. (Always more, always faster, but even then, not always better).

However, this usage of AI predominantly fixates on the creation of additional data, guided by the assumption that more data processed inherently leads to more superior outcomes.

We reside in an age of data abundance. We cannot forget that not all data is created equal. We must recognize that the effectiveness of AI is contingent upon the quality of the data it encounters.

This distinction between data signals vs. noise becomes pivotal when crafting algorithms designed for credit or investment decisions If the input data is tainted with any noise or bias, the AI's output will inevitably mirror these deficiencies.

The key failure in our industry’s current approach is this failure to recognize that our data quantities aren’t the issue for more assured decisioning. Rather, we should be in pursuit of distilling data down to its most truthful forms to direct algorithms with better, verified inputs with the power to tell the story we’re actually trying to understand.

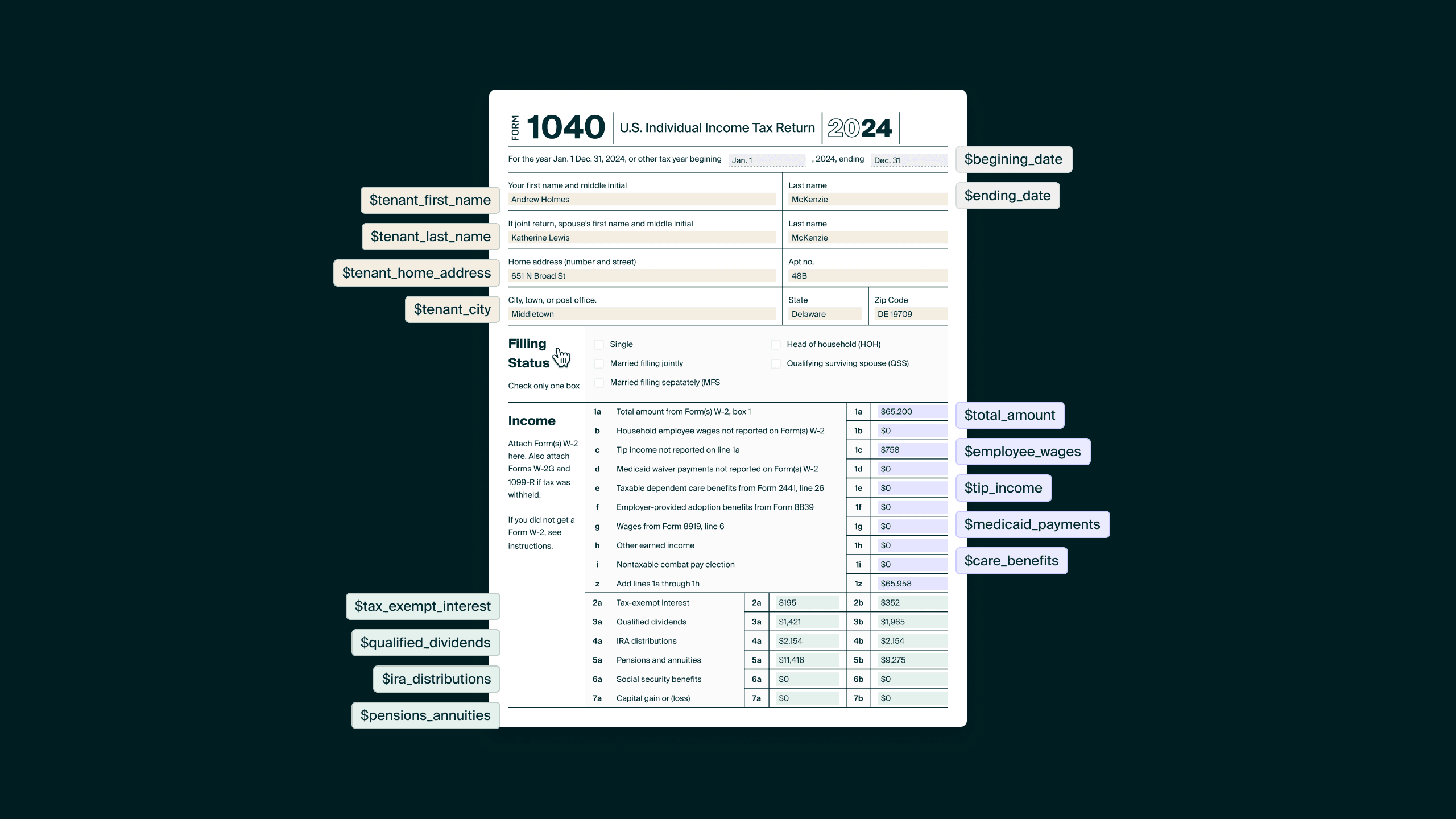

A first step to accurate data inputs is to shift away from the current practice of working with financials that are self reported, therefore subject to biased, opaque, or misleading influence.

When it comes to discussions surrounding machine learning for financial decisioning, there is an often-raised question: why not simply use AI to comb through legacy platforms housing “millions of SMB’s financials” like QuickBooks, or Bloomberg?

It is paradoxical to entertain the idea of AI independently making financial decisions while credit teams still rely on self-reported data (in this context, borrower supplied or pre-calculated financial data taken as fact).

The enormous variance in approaches to financial reporting, the significant potential for human error, and the unreliability of unverified information undermines the reliability of any decisions based on self reported financials.

Let’s consider this concept in practice.

An SMB borrower is applying for financing. The borrower provides their bank a suite of financial statements and documents, some created in Quickbooks, others assembled by the SMBs employee, and still other financial documents from their own files.

Did the SMB set up their system to perform accounting cash-basis, or on an accruals-basis? Is their general ledger configured the same as other similar business types? How does this business calculate their COGS and profitability differently?

And even if an underwriter works hand in hand to understand exactly how each item was calculated, how do they verify that data? Can they?

These questions of data integrity in automated decisioning shape our goals for developing decisioning infrastructure rather than playing into the existing generative AI paradigm.

Understanding data origins and how calculations have been made, combined with the imperative to standardize and verify it, underpins the very foundation of building blocks to successful algorithmic financing decisions.

This is why we do not seek to augment customer financials with more and more. Our aim is to instead create the tools and processes for extracting meaningful insights from the existing data reservoir.

The approach we’ve taken for this at SOLO hinges on developing intricate processes of deconstruction, verification, standardization and the extraction of profound insights from raw data. Ensuring truth goes in, so that trusted decisions can come out.

In this process, a customer’s financials should be:

The insights mined, in turn, are the bedrock powering informed decision-making. We refer to this as a shift from self reporting to autonomous reporting.

In this approach, the data harnessed for our decisioning algorithms isn't merely abundant but is verified as true at the very start in how it exhibits value, accuracy, and structural soundness – elevating the overall decision-making process into an outcome worth banking on.

What would the methodology of an automated decisioning process built on autonomous reporting look like in more specific terms?

Let’s consider our SMB borrower once again. But this time, through the process we’ve established for the autonomous deconstruction to reconstruction of data then used for automated decisioning.

Data collection should be secure, verified, and standardized in a seamless data collection infrastructure. Permissioned data (information access granted expressly by the user) enhances a decisioning algorithm’s reliability. Data calculations can then, and only then, be ensured as accurate and authorized down to each individual point of raw data.

At this stage, our potential borrower would apply through a financing application with primary data sources integrations granted by a login connector.

The user would give secure permissions to access accounts, like bank accounts, Quickbooks, point of sale platforms, contract management software, in addition to others.

Importantly, this access would not just grant visibility into finished financial statements but into the live millions of data points feeding into those engines. We need to be collecting the entire web of live customer data.

Data and can then be seamlessly collected into a reporting engine to begin deconstructed, with a traceability that inherently verifies accuracy at the most basic level.

Once securely collected and made traceable, data must now be standardized into a meaningful language universally understood: financial statements calculated to the exact standardizations of the deciding entity.

At this stage, our SMB borrower has no burden to produce documentation, and neither does the underwriter. This is where automation can actually begin to revolutionize a bank’s process with a level of radical transparency, in the right reporting engine.

Trust should be established through visibility into the reporting results with the ability to view every data source, calculation, and result.

{Product Tour Preview Embed: How we do this in SOLO?}

Once data is collected, verified, traceable, and standardized, then automated decisioning algorithms can confidently be applied.

Financials at this stage will reflect the real methodology of a bank or lender’s underwriting process, so inputs collected and calculated are actually trusted as fact.

In this framework we argue that automation can be applied constantly to live data, as long as accounts remain connected.

This is where we’ve been experimenting with decisioning for radical transformation in the approvals process. SOLO is testing a hypothesis of automated continuous underwriting’s viability in comparison to the standard decisioning model assessing point in time credit risk.

Currently, a lender must underwrite every product application instance for each customer. The scoring framework is static and retrospective, with underwriting costing a bank hundreds to thousands per customer per financing application.

We are building a system powered by automation where the cost to underwrite is dramatically reduced, with the timeline for gauging creditworthiness upon customer acquisition is extended to 365 days on all the bank’s products.

In this model, our SMB borrower is given a period of 365 days and an actionable plan for how to qualify for a specific financial goal dependent on credit calculations that are most relevant to their desired financing product. Automated decisioning, plus first party data permissioning, recenters transparency as a tenet of banker-lender trust and a proponent of a more competitive open banking field.

What artificial intelligence has yet to do successfully is develop an automated intuition that doesn’t just mimic human intuition, but provides us with a completely novel trust in its decisioning power.

The beauty in autonomous reporting, once the concept is adopted, is its future power. There may be an ability to unlock new signals that capture credit potential in a way more closely resembling the human intuition that is a trademark of the best investors.

Imagine our borrower is a startup. Incentivized correctly, they may be prompted to connect all their operating systems including unconventional sources for financial data, like Slack, calendars, emails, GitHub, CRM, marketing tools, website analytics, project management systems and more.

What could these data sources tell us about how a business would respond when they are running out of runway?

Do they increase ad spend to try to optimize revenue, or do they conserve spend and die slowly?

These are all data points you can get by deconstructing, that investors spend weeks trying to answer. Behavioral analytics can be derived from verified data sources if reporting is done autonomously with no human interference.

Our long-term mission for how we use AI revolves around harnessing machine learning to construct an intelligence layer, leveraging both financial and non-financial operational data sourced from our existing revenue-generating business-oriented product. This non-financial data encompasses a diverse range of metrics for uniquely modern businesses that. Amalgamating these data points, we transform the intangible assets of the internet economy into quantifiable financial indicators, a resource that investors can wield to inform their decision-making processes.