BlogOct 20, 2025

In our framework credit becomes a shared language, transformed from a single score, into a single source.

What does it take to build a collaborative credit bureau, where trust is earned at every step?

Credit scoring is essentially an attempt at measuring trust based on a standardized aggregated of verified identity, behaviors, and probability of one's ability to deliver on a promise.

But we believe trust extends beyond verification and oversimplification.

Attempts to quantify trust through credit metrics have become overly standardized, static, and outdated for the modern world. A single score may have worked in the 80s. It's now just a small piece of one's credit identity.

Rather than an overly standardized, static calculation we believe in a framework that fosters a shared language between stakeholders, where the meaning of credit data is defined by each decision-maker, and universally understood to convey true meanings for each unique person and context.

The banking industry’s approach to credit assessment has been to take fragmented, unstandardized inputs—pieces of the story—and produce one standardized assessment that’s applied universally, like a single score or a spread.

Our approach is fundamentally different: we standardize at the input level, creating one clear source of truth that allows for multiple customized conclusions/flexible spreading for every context.

This enables context-driven assessments tailored to each unique situation. In essence…

SOLO: one source of truth, many lenses and conclusions.

Industry: fragmented, unstandardized parts of the story forced into a single, one-size-fits-all assessment.

The technical difference? It’s all about when standardization happens.

For others, it’s at the output level. For us, it’s at the input level.

We talk a lot about this methodology in our conversations on shifting from self reporting to autonomous reporting for collecting customer financials at the beginning of a financing application. In this method data can be transformed from an aggregation into individualized activations for each product and risk environment.

It's possible in a framework that puts the focus on a decisioning model's inputs, shifting the burden of financial calculations off customers and the underwriters charged with verifying them (often rebuilding them from scratch to fit a specific credit box).

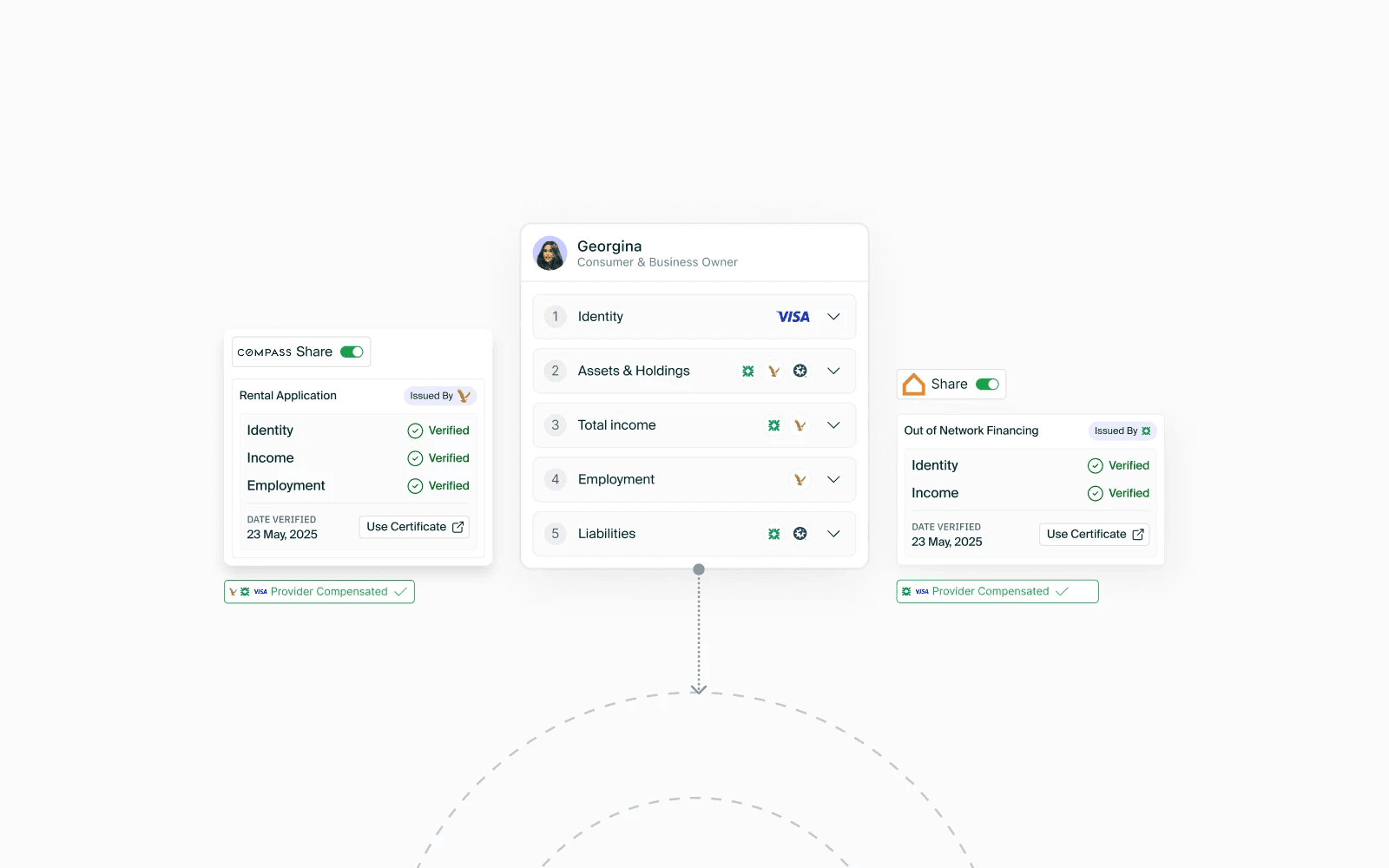

The OneTrust framework creates a “record of truth” for each consumer. SOLO allows users to own their credit data, while banks query the data they need in real time, optimizing both efficiency and customer experience. The result is a shared language of credit, eliminating the back and forth between customer and banker to put all parties on the same page at first introduction.

By connecting and transforming raw data into tailored profiles — unique to each bank, product, and risk profile — we can ensure that many stakeholders see the same data while enabling them to interpret it through their own lenses.

This framework paves the way for dynamic credit scoring models, allowing lenders to customize credit scores based on attributes that matter to their specific products.

At the same time, it provides consumers with transparency, showing them tailored scores that align with both their unique financial circumstances and the specific risk preferences of each institution.

By aligning the perspectives of both consumers and lenders, this shared language enhances the relevance of credit assessments, enabling more precise, context-driven decisions for both parties. Only then can the truth in data be universally understood.

SOLO’s credit bureau is powered by this reporting engine: one that enables the ingestion of data from any source while giving lenders control over how the data is calculated and interpreted. Our framework is built to support this process.

Trust begins through verification and shared language. Consumers provide raw data, and lenders determine how to calculate and interpret it.

This is the future of trust: moving from a fragmented, oversimplified, and siloed view of consumers to a unified, raw, and constantly evolving ledger that gives each institution the freedom to interpret and calculate trust based on their unique needs and context.

It's not about one number ruling all, but about empowering financial institutions to see individuals for the full, nuanced, and dynamic entities they truly are.

Trust is not earned with every new interaction but is granted through a living, breathing system of record, built on shareable and reusable data assets. This system shows a complete picture of an individual, which can be standardized for decision-makers.

What makes sense now, in a world of dynamic and individualized financial landscapes, is a Unified Ledger of identity, activity, relationships, and financials—a raw, living system of record. This ledger serves as a 360-degree, holistic view of a person’s financial life, not confined by arbitrary data silos.

The data in this ledger isn’t pre-packaged, pre-concluded, or predetermined by an outside party.

Instead, it’s raw, meaning that every bank, lender, or institution can interpret it in their own way. They have full control over the calculations and standardizations that go into creating individualized scores, tailored to the specific context, product, and risk profile they are dealing with.

Trust extends by leveraging the credibility of other trusted financial stakeholders in the ecosystem. Institutions can base decisions on shared relationships with these stakeholders.

Trust is bolstered by involving highly specialized third-party systems that can contribute their expert data to specific decisions.

For instance, when a pool contractor applies for a working capital loan, a specialized service like Skimmer could provide data on the income potential of related construction projects based on the pool’s asset history.

Lenders can call upon these expert databases or even license specialized frameworks to enhance decision-making. This creates a collaborative risk ecosystem, where specialized groups can participate in both origination and collections.

Scores in our framework become nothing more than lenses —different perspectives through which each financial institution can view a consumer, attuned to the specific context, product and institution's risk preferences. No additional verification needed.

The OneTrust Framework was created to move from a broken system where one overly simplistic score rules all decisions, to a future where each consumer is seen as a dynamic, evolving entity.

This Unified Ledger concept enables financial institutions to create trust in a way that is as complex and nuanced as the lives of the individuals they serve.

Consumers are no longer reduced to a single number that doesn't account for their specific circumstances or the products they’re applying for. Instead, they become the owners of a living financial profile—a Bureau of One—where their identity is reflected in the diversity of scores created by different institutions. It’s about moving away from over-standardized assumptions to context-driven, customized evaluations.

With the Unified Ledger acting as an individualized but universal record of truth, we’ve replaced one static score with one dynamic profile interpreted in infinite ways—creating a financial ecosystem that is more personalized, adaptive, and fair for everyone involved.

Scores in our system become nothing more than lenses—different perspectives through which each financial institution can view a consumer's true financial identity, but never the whole story.

For example, where overly standardized scores might reduce someone to a 635 across the board, we propose that same consumer could score a 762 at a bank for a mortgage, precisely because the score is attuned to the specific product and institution's risk preferences.

In the 1980s, lenders relied solely on a single standardized score to underwrite consumers for credit cards, making decisions based on that single number.

However, today, a single score only takes you part of the way. Additional attributes and features from an application are required to align with a bank’s specific risk policies for particular products.

These factors collectively inform the final decision, with credit scores now serving more as an approximation rather than a definitive measure.

The OneTrust Framework paints the rest of the picture.

In the wake of the Consumer Financial Protection Bureau's final rule on Personal Financial Data Rights (CFPB Final Rule 1033), even the smallest banks and institutions must be ready to become both data provider and receiver.

They must also be ready to equip their customers with complete access, permissioning power, and monitoring of their data.

We've developed SOLO's framework to act as a tool for protecting and controlling access. Individuals and businesses would have control over what information is shared with whom, for how long, and for what purpose. This would allow for public-facing data when needed, but also for more secure, limited sharing with specific institutions for specific timeframes or purposes.

In this system the user maintains complete permissioning control over their financial identity and its interactions across multiple institutions.

Ultimately, our framework creates a foundational layer where every ID and transaction—whether individual, business, payment, or onboarding—flows through a secure, verifiable ledger.

But it's more than that.

We're creating a dynamic, evolving system where trust is built incrementally, layer by layer, through real-world verifications and activities where consumers control their permissions.

We see our role at SOLO as a base layer of financial trust and identity, tying together the disparate elements of the current system into one interconnected, secure framework to move from one inconclusive score to 1 ledger with 100 conclusions.

Georgina Merhom is the founder and CEO of SOLO, a collaborative credit bureau that transforms how first party data is collected, verified, and activated for banks and lenders. Prior to SOLO, Georgina began her career as a researcher and compliance director at the G7 & G20 Information Centre. She then trained as a data scientist and investigative analyst to develop algorithms that detect illicit activity on the dark web. In 2020, Georgina founded Zivmi, Egypt's first cross-border payments app, in partnership with the National Bank of Egypt, providing invoice factoring to unbanked digital freelancers. She subsequently exited the venture in its entirety to the National Bank. Through her work with unbanked freelancers at Zivmi, Georgina recognized the limitations of traditional credit assessment which led to the creation of SOLO and her advocacy for modern solutions in credit and lending.