Mick Mulvaney Joins SOLO

SOLO Names Mick Mulvaney Advisory Board Chairman as FICO and JPMorgan Turn Against Data Intermediaries, Signaling a Shift in How Trust and Credit Are Built

SOLO Names Mick Mulvaney Advisory Board Chairman as FICO and JPMorgan Turn Against Data Intermediaries, Signaling a Shift in How Trust and Credit Are Built

As first reported by PoliticoPro.

SOLO, a rapidly growing customer data sharing network backed by more than 100 community and regional banks, announced the appointment of Mick Mulvaney, former Director of the Consumer Financial Protection Bureau (CFPB), Director of the Office of Management and Budget (OMB), and White House Chief of Staff, as Chairman of its Advisory Board.

Mulvaney joins SOLO at a pivotal moment for the financial services industry, as the nation’s leading financial institutions are making drastic changes due to the failures of credit bureaus and leading aggregators.

Recent announcements include FICO now bypassing legacy credit bureaus with a new direct mortgage score program and JP Morgan pushing the fintech middleman Plaid to pay for access to their bank-validated customer data.

As SOLO’s collaborative customer data network emerges as the leading alternative to legacy credit bureaus and data aggregators who have failed to meet the needs of the open banking era, Mulvaney’s decision to join the leadership team of the rapidly growing startup underscores a broader industry reckoning: the credit bureaus and traditional data intermediaries can no longer meet the demands of a rapidly evolving financial ecosystem.

SOLO’s data sharing network represents the permanent, consumer-first alternative.

“The largest financial intermediaries like Plaid and the largest credit bureaus were built for a different era, and they’re holding us back,” said Mick Mulvaney. “These organizations are profiting off of inefficiency and systemic silos and they fail to represent the full scope of consumers’ financial lives. SOLO’s technology and protocol will enable the future of real open banking, where individual data is comprehensive and portable, and institutions are compensated for validating financial information. SOLO’s network reflects the world we live in now, not the one we are leaving behind.”

“Director Mulvaney’s conviction in SOLO stems from our shared belief that the infrastructure of consumer data is falling apart and that the future depends on collaboration and incentive alignment that puts financial institutions and consumers on the same side,” said Georgina Merhom, founder of SOLO.

“When the largest aggregator in the industry agreed to start paying the largest bank, it marked more than a business deal, it was an admission that the old version of open banking is obsolete. Weeks later, FICO cut the credit bureaus out of its scores, confirming what everyone already knew: ad hoc negotiations on data sharing can’t govern the infrastructure that decides who gets access to a loan, a job, or a place to live. These are not surface-level disputes but rather a structural collapse. The industry has outgrown its patchwork of private arrangements and needs a shared protocol.”

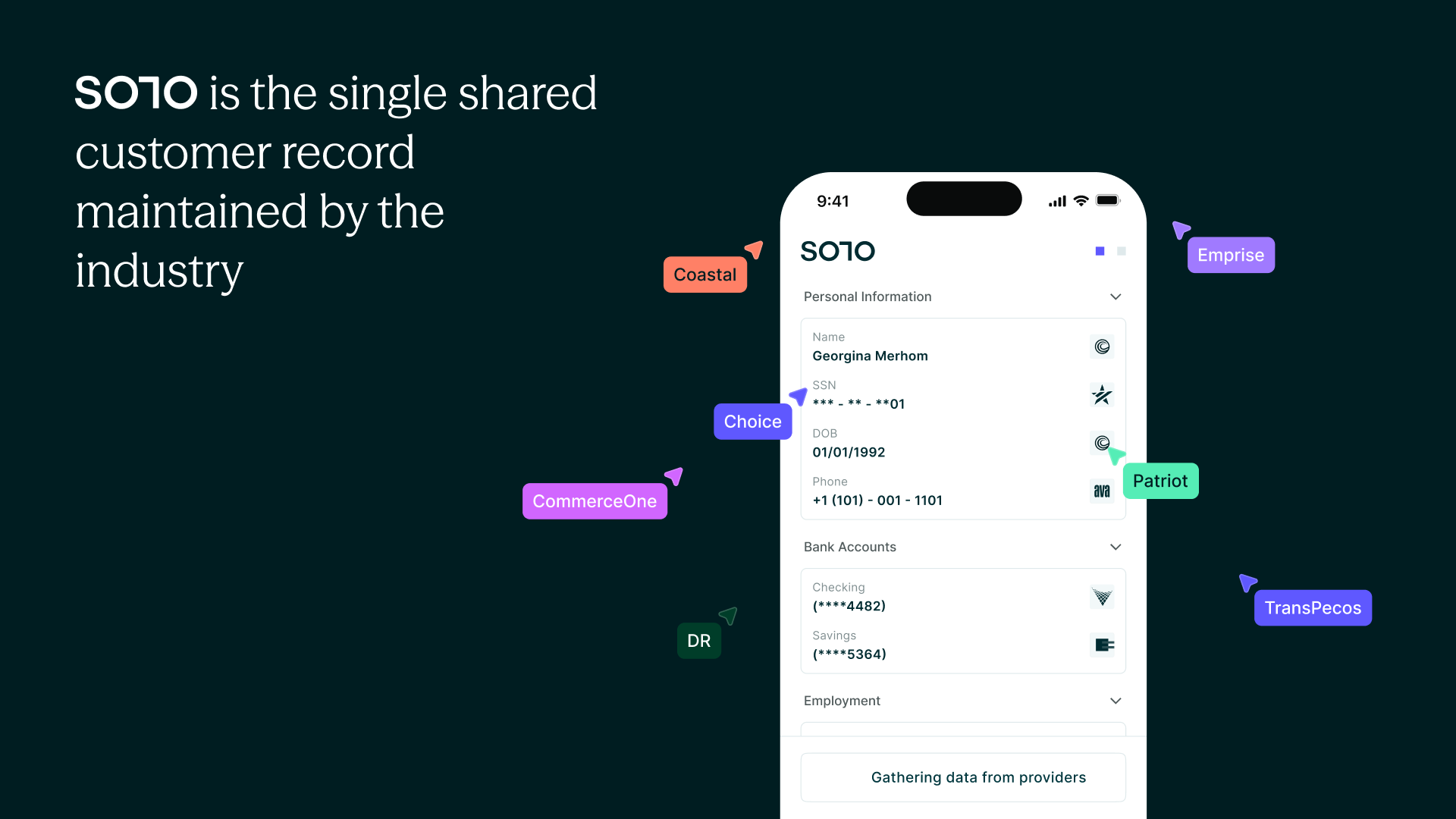

SOLO’s one-click consent model replaces the patchwork of fragmented solutions that force consumers to repeatedly prove themselves to every new provider. Instead, it enables trusted data sharing with a single authorization — compensating the banks, fintechs, and partners who contribute verified information and vouch for the customer.

SOLO rejects the outdated architecture built by legacy credit bureaus and aggregator led web scraping.

For too long, data middlemen have profited from fragmentation and redundancy at the expense of the consumers, institutions, and fintechs they claim to serve, capturing only fragments of consumer profile truth and then selling that data back to the very industry that produced it.

Instead, SOLO’s network participants are all incentivized to contribute to a consolidated customer profile.

Data is stored atomically and travels with its compliance history directly across institutions.

Customers control access.

Institutions control how data is used, and are compensated when data they provide is reused throughout the network.

By replacing data hoarding with collaboration, SOLO rewards every participant for compliant data collection, relationship building, and maintaining the consumer’s verified record — creating a network where helping the customer is also good business.