BlogOct 20, 2025

A deep dive into the architectural shifts SOLO's infrastructure brings to open banking, as seen in This Week in Fintech.

This article is excerpted from its original publication by This Week in Fintech.

The Dodd-Frank Section 1033 debate in the US is the latest to highlight that consumer data access– whether in financial or non-financial contexts– is subject to questions around who bears the commercial and legal liability for provisioning data.

Zoom out from the open banking debate and there's a bigger question at play: How can we unlock consumers' rights to access all of their data, in every context where it needs to be shared?

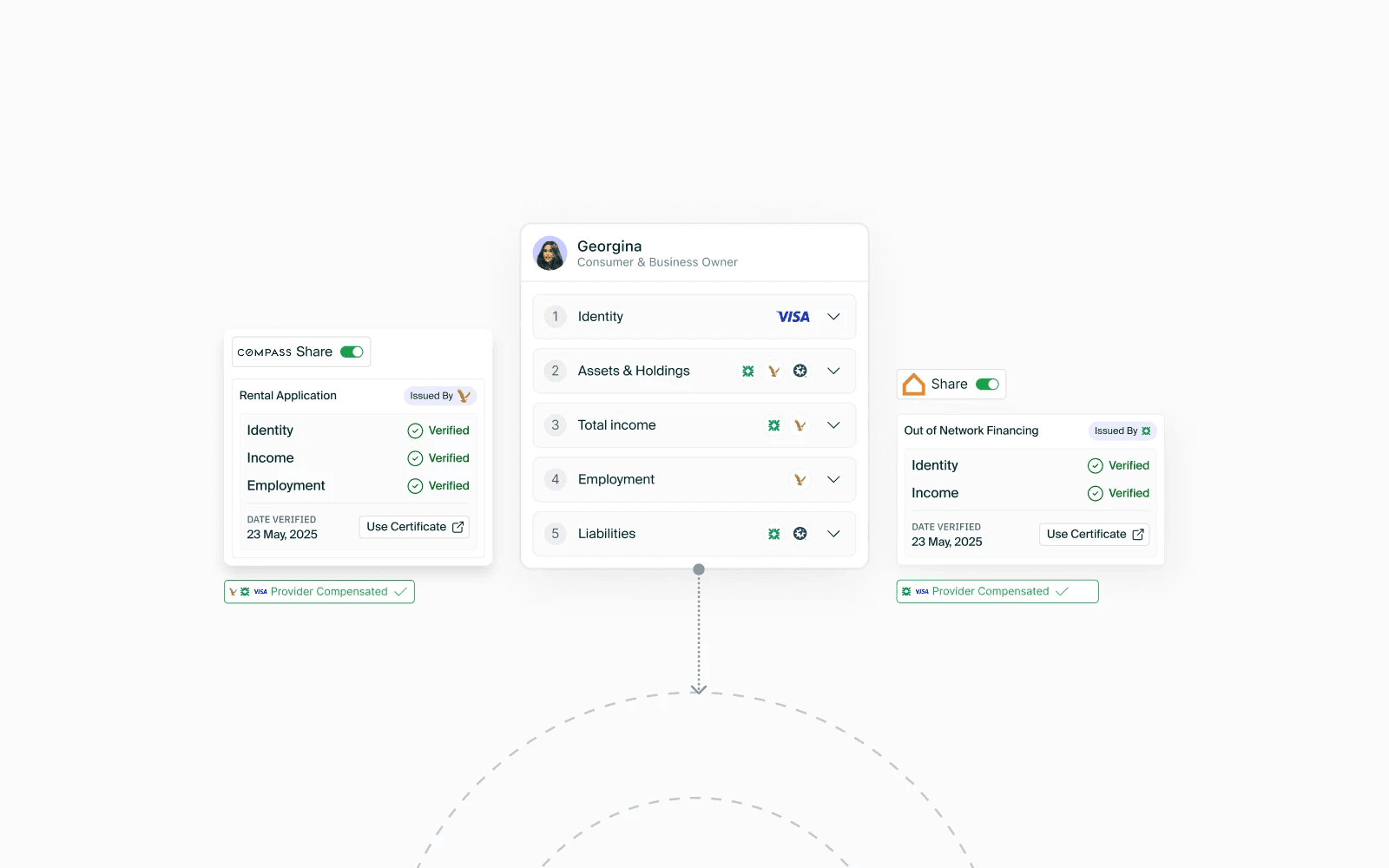

Platforms like SOLO demonstrate how a user-permissioned data sharing network can tackle this question to operationalize trust at scale. SOLO enables all open banking participants– from financial institutions to fintech platforms– to access and contribute a wide range of data to a single source of truth on a shared customer. The data becomes portable across the network, with sharing controlled by the end user and usage controlled by the financial institution or fintech platform for their specific workflows, compliance protocols, and products.

Interestingly, SOLO shifts the data furnishing model by enabling financial service providers to be compensated for contributing to users' data– incentivizing data furnishers to maintain and share verified information across network participants. Launched earlier this year, the network is projected to cover 100 million consumer profiles through its existing partnership contracts by the end of 2025.

Let's dive into the evolution of data portability, how the industry is shifting, and how networks like SOLO rearchitect data sharing for the next era of data access in finance.

Early credit files emerged in the 1800s with local shopkeepers pooling purchase logs to assess customers' creditworthiness. When vendors held different fragments of customers' financial data, centralized credit files enabled trust.

In the past few decades, the Fair Credit Reporting Act enforced standards for credit reporting and later on, the Dodd-Frank Act Section 1033 established consumers' right to access their own data from financial institutions. Open banking APIs and fintech credit bureaus built on these regulations to unlock direct access to user-permissioned data. Meanwhile, financial institutions took steps toward industry-wide knowledge graphs with consortiums like Early Warning Services, DTCC, and The Clearing House's fraud databases– and more recently, fintech infrastructure players launched their own consortiums like Plaid Beacon and Sonar to pool risk signals from more tech-enabled players.

These shared datasets expand visibility beyond single institutions, but each covers a narrow range of data fields and data typically flows in one direction: Out of regulated institutions. The broader constellation of data contributors and platforms accessing their information still lacks incentives to collaborate on a persistent, holistic, single source of truth that can be accessed across institutions.

"Open banking ten years ago assumed that all the data lived in the banks," explains Georgina Merhom, Data Scientist and Founder of SOLO. "Banks were seen as providers of data and fintechs were consumers of data. The reality now is that both banks and fintechs can be consumers and providers of data. We've moved away from needing one directional data portability to an ecosystem where trust can move both ways."

Today, our financial lives don't fit neatly into the old categories. Your "primary" financial relationship might be with your bank, but meaningful data also lives with your BNPL provider, your accounting provider, your budgeting app, your rent payment platform, and your eCommerce gateway.

But lenders' policies, compliance frameworks, and technical systems aren’t engineered for that data to flow freely from your bank to fintech providers and back again. Credit bureau files and bank data feeds carry implicit credibility since regulators enforce compliance with strict processes– but repayment data originated by fintechs, BNPL platforms, or payday lenders outside that traditional regulatory perimeter doesn’t come with audit trails to verify its provenance or data governance.

Meanwhile, every financial provider builds their own user profiles from scratch– even when existing relationships could provide valuable information for customers accessing new services – so financial platforms may end up using 10+ onboarding vendors to screen new applicants' information across thousands of databases for financial data, KYC, AML, fraud, and credit checks…

All for users to re-verify the same information every time they sign up for a new service.

Platforms like SOLO are rethinking data sharing for a world where financial institutions, fintechs, and other data providers are peers in an ecosystem.SOLO is the first network-powered bureau built as a relationship engine– dynamically interpreting workflow context, identifying the specific data elements required, and resolving gaps in financial datasets by orchestrating inputs from both the customer and the network.

As a living, multi-directional network, SOLO’S utility compounds as new customer context is added. Every interaction enriches the network, enabling faster onboarding, more accurate resolution, and a continuously expanding surface of usable data.

The key architectural shifts behind SOLO:

For fintechs and financial institutions, collaborative networks enable:

SOLO is backed by 100 banks and has both banks and fintech programs participating in its network; as the network scales further, the potential for market-driven collaboration to enable consumer data access compounds.

The future of data sharing isn't about building new static information archives. It's about building networks where everyone can contribute, everyone can consume, and users control what gets shared in real-time.

Interested in learning more about SOLO's network model for data sharing? Contact SOLO.