TechCrunch: SOLO’s new credit bureau concept helps lenders ditch third-party data

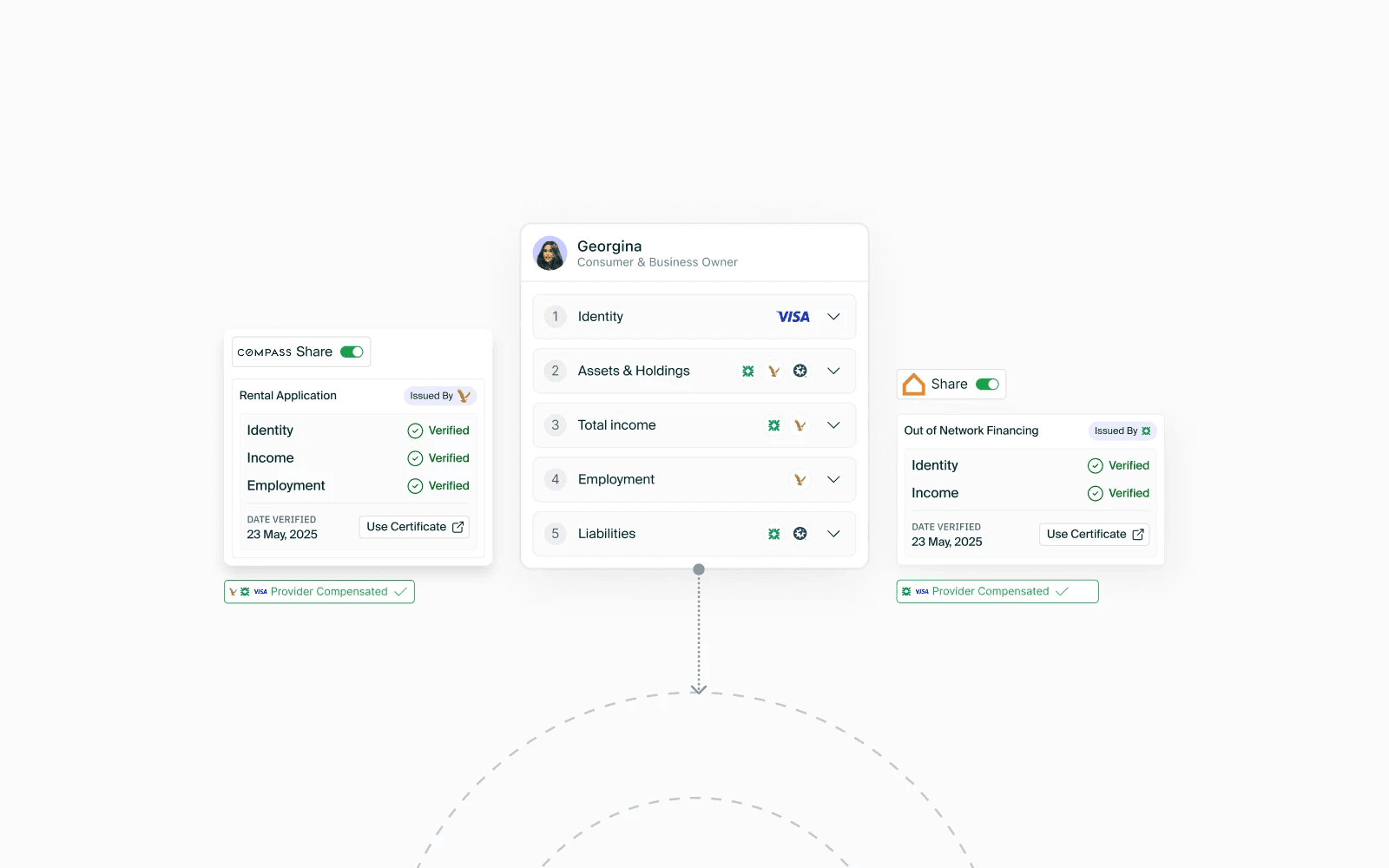

SOLO’s new collaborative credit bureau concept transforms how customer financials are collected and activated for lenders.

SOLO’s new collaborative credit bureau concept transforms how customer financials are collected and activated for lenders.

Excerpted from TechCrunch.com

Credit bureaus relying on outdated third-party data are only getting a small piece of the puzzle, Georgina Merhom says.

“The credit bureaus are super relevant, but when it’s used to identify that a person didn’t pay one bill on time, it’s a punishment. If you are only following the money, you can miss out on a lot of signals,” Merhom told TechCrunch.

Merhom wants to squash the status quo with SOLO, a first-party data collection and reporting engine, that integrates user-permissioned data sources, including financial transactions, online records and digital footprints to tell a more complete story about someone’s financial behavior.

User-permissioned data sources, that consumers provide with their permission, come from a variety of places. This includes bank accounts (via Plaid, Teller, TrueLayer), commerce and payment gateways (Amazon, Shopify Square, Stripe, PayPal), invoicing/billing systems (QuickBooks, Bill.com) and customer relationship management platforms, Merhom said.

In addition, user-permissioned data sources replace the self-reporting process, brokers trust between the institution and consumer and identifies opportunities that the bank would have otherwise overlooked, Merhom said.

Originally a data scientist in the cybersecurity industry, Merhom was developing and training algorithms on the dark web to detect illicit activity. That work taught her that a wider variety of data, as well as the context in which the data appears, can paint a much fuller picture. Merhom used that intelligence to start Zivmi, a cross-border payments app in Egypt that she ended up selling to the National Bank of Egypt.

She got the idea for SOLO while at Zivmi and working with freelancers without bank accounts. Using other platforms like GitHub and Upwork, Zivmi was able to verify a person’s experience level, client ratings and overall work history.

As the business of working with the unbanked grew, Zivmi started underwriting its customers and developed the technology to do that. Merhom said that’s when she recognized the need to create a new kind of credit bureau…

Read the full feature at techcrunch.com