Index

CATEGORY

Best Practices

Launch a Digital Lending Platform (Updated 2025)

Scaling a digital lending platform requires reliable software for automating onboarding to underwriting. This roadmap outlines the critical comonents of launching a digital lending platform.

Dec 5, 2024

In today’s financial landscape, digital lending software has become a cornerstone of modern banking, enabling lenders to streamline processes, enhance customer experiences, and improve efficiency. This guide explores the critical components, technical foundations, and clear roadmap for launching digital lending software with best practices updated for 2025 and beyond.

What Is Digital Lending Software?

Digital lending software is a suite of tools and platforms that facilitate the end-to-end process of managing loans, from application and underwriting to approval and disbursement. Unlike traditional lending processes that rely heavily on manual tasks, digital lending leverages automation, advanced analytics, and integration to deliver faster and more accurate decisions while reducing operational overhead.

Components of Digital Lending Software

Loan Origination System (LOS):

Manages the intake and processing of loan applications.

Automates workflows for application review, data validation, and document collection.

Dynamic Credit Scoring and Risk Assessment Module:

Evaluates borrower creditworthiness using internal and external data.

Employs bank controlled metrics to measure risk.

Document Management System:

Centralizes storage and retrieval of borrower documents.

Enables e-signatures and digital compliance tracking.

Underwriting Engine:

Automates decision-making using predefined rules and machine learning models.

Allows manual intervention for edge cases or exceptions.

Compliance and Audit Tools:

Ensures adherence to local and international regulations (e.g., GDPR, FCRA).

Maintains audit trails for transparency and accountability.

Loan Servicing Platform:

Manages post-approval activities such as payment collection and reporting.

Integrates with payment gateways and accounting systems.

Customer Relationship Management (CRM):

Provides a seamless interface for borrower communication.

Tracks borrower interactions and preferences to enhance service delivery.

Why Was Digital Lending Software Created?

The emergence of digital lending software is rooted in the need to address inefficiencies and challenges in traditional lending systems:

Manual Processes: Traditional workflows were labor-intensive and prone to errors.

Customer Expectations: Borrowers increasingly demand quick, transparent, and digital-first experiences.

Regulatory Complexity: Ensuring compliance manually was time-consuming and error-prone.

Data Utilization: Advances in data analytics and machine learning created opportunities to leverage vast datasets for better decision-making.

By digitizing the lending process, these tools enable financial institutions to meet modern demands while staying competitive in a rapidly evolving industry.

How Digital Lending Software Works

1. Application Submission: Borrowers initiate the process through an online portal, submitting personal, financial, and loan-related information.

2. Data Integration: The software pulls information from multiple sources, such as credit bureaus, financial statements, and alternative data providers, to verify borrower details.

3. Risk Assessment: Using advanced analytics, the software evaluates the borrower’s creditworthiness and assigns a risk score based on factors such as credit history, income stability, and industry trends.

4. Underwriting Decision: Automated underwriting engines analyze the data and provide decisions based on predefined rules. Exceptions are flagged for manual review by underwriters.

5. Document Management and Compliance: Borrower documents are securely stored, verified, and tracked for compliance. E-signatures are used to expedite agreement processes.

6. Loan Approval and Disbursement: Upon approval, the system facilitates loan agreement generation and fund disbursement through integrated payment systems.

7. Loan Servicing and Monitoring: Post-disbursement, the software manages payment schedules, collections, and delinquencies while providing real-time monitoring of loan performance.

The Digital Lending Roadmap: How to Launch a Digital Lending Platform with SOLO

Examining the pain points of bankers and frustration with traditional digital lending platforms, SOLO developed a technology and philosophy around digital lending to address the needs of the industry with the expertise of our team’s data science foundations.

We believe a truly reliable digital lending platform begins with establishing a system to prevent inaccuracies in automated decisions by shifting focus back to the very beginning of the lending process.

Algorithmically determined decisions are only as reliable as the inputs used within them. The finer points of the Digital Lending roadmap stem from our core philosophy of data collection and governance within digital lending.

To create a credit infrastructure that can automatically translates credit data into its most meaningful forms, we must first ensure that the meaning of data is truthful, verified, and properly understood at its very basic unit before being standardized, consolidated, and reinterpreted for credit algorithms.

Fundamentals: Data Collection is Critical

It is crucial for digital lending platforms to shift focus from decision outputs to data ingestion, standardization, and reinterpretation into the true meaning of financials within the context of the lender’s credit appetite.

An automated decisioning should be the result of a reporting engine that enables the ingestion of data from any source, while giving lenders control over how the data is calculated and interpreted.

In this model the burden of financial calculations shifts away from customers, who traditionally self-report information in a way that’s still too open to interpretation by a lender to be truly useful.

Instead, raw data aggregation leads to individualized activation for each product and risk environment.

This creates a scalable system to build a shared language of credit, eliminating the back and forth between customer and banker to put all parties on the same page at first introduction with verified data, made accurate for the context of decision makers.

By connecting and transforming raw data into tailored profiles — unique to each bank, product, and risk profile — a digital lending platform powered by such a framework ensures that many stakeholders see the same data while enabling them to interpret it through their own lenses.

After this infrastructure is built, and only after it’s built, the framework paves the way for dynamic and automated credit scoring models, allowing lenders to rely on the accuracy of customized credit scores based on attributes that matter to their specific products.

We believe this should be the true goal for any lender seeking a reliably automated lending platform.

The Stages of Building a OneTrust Framework

1. Replacing Self-Reporting with Autonomous Data Collection

Trust begins through verification and shared language. Consumers provide raw data, and lenders determine how to calculate and interpret it.

This is the future of trust: moving from a fragmented, oversimplified, and siloed view of consumers to a unified, raw, and constantly evolving ledger that gives each institution the freedom to interpret and calculate trust based on their unique needs and context.

It's not about one number ruling all, but about empowering financial institutions to see individuals for the full, nuanced, and dynamic entities they truly are.

2. Create a 360° Profile

Trust is not earned with every new interaction but is granted through a living, breathing system of record, built on shareable and reusable data assets. This system shows a complete picture of an individual as a Unified Ledger of identity, activity, relationships, and financials—a raw, living system of record.

The data in this ledger isn’t pre-packaged, pre-concluded, or predetermined by an outside party.

Instead, it’s raw, meaning that every bank, lender, or institution can interpret it in their own way. They have full control over the calculations and standardizations that go into creating individualized scores, tailored to the specific context, product, and risk profile they are dealing with.

3. Trust by Proxy Through Other Financial Stakeholders

Trust extends by leveraging the credibility of other trusted financial stakeholders in the ecosystem. Institutions can base decisions on shared relationships with these stakeholders.

4. Enable a Deep Understanding of Credit by Developing Context

Trust is bolstered by involving highly specialized third-party systems that can contribute their expert data to specific decisions.

Lenders can call upon these expert databases or even license specialized frameworks to enhance decision-making. This creates a collaborative risk ecosystem akin to community banking’s traditions, where specialized groups can participate in both origination and collections.

Prioritization Matrix: Identify Where to Begin

We found that, although a full end to end solution may be the best future state for one lender, others may be mid-revamp of existing systems. In these cases, priorities needed to reflect the progress and the ambitions of the bank for incremental growth.

Before launching a digital lending platform, Lenders should consider:

What type of financial data does the bank currently leverage to make product decisions with? What’s missing?

Are your underwriting teams able to keep pace with demand?

Has it been a challenge to create or tap into demand in your market? How application conversion tracked, and what number indicates ‘success’?

What is your current or near-state tech stack? Are these performing to the expected degree? How would you like a digital lending platform to connect with or replace pieces of this tech stack?

How are you identifying expansion opportunities with your customers? What are your growth goals this year and how are you planning to achieve them?

How are your lending / sales teams leveraging financial data to grow the LTV of their portfolio?

Use these questions to asses top priorities. Many of our lenders cite the following goals as their key priorities for a digital lending platform:

Streamline Verified Data Collection

Scale Underwriting Bandwidth

Optimize Lead Conversion

Integrate Tech with Existing Systems

Identify Customer Expansion Opportunities

Improve Profitability of Loan Products

Many of these priorities are interconnected, so improvements in one area will inevitably impact others. A well defined priority provides a clear beginning point for a banks to launch a digital lending platform, but it is just that. A beginning.

This process takes repeated iterations, experimentation with A/B testing, and trial and error over time to optimize revenue potential within a digital experience.

Digital Lending Roadmap to Address Primary Pain Points:

1.) Priority: Scale Underwriting Bandwidth.

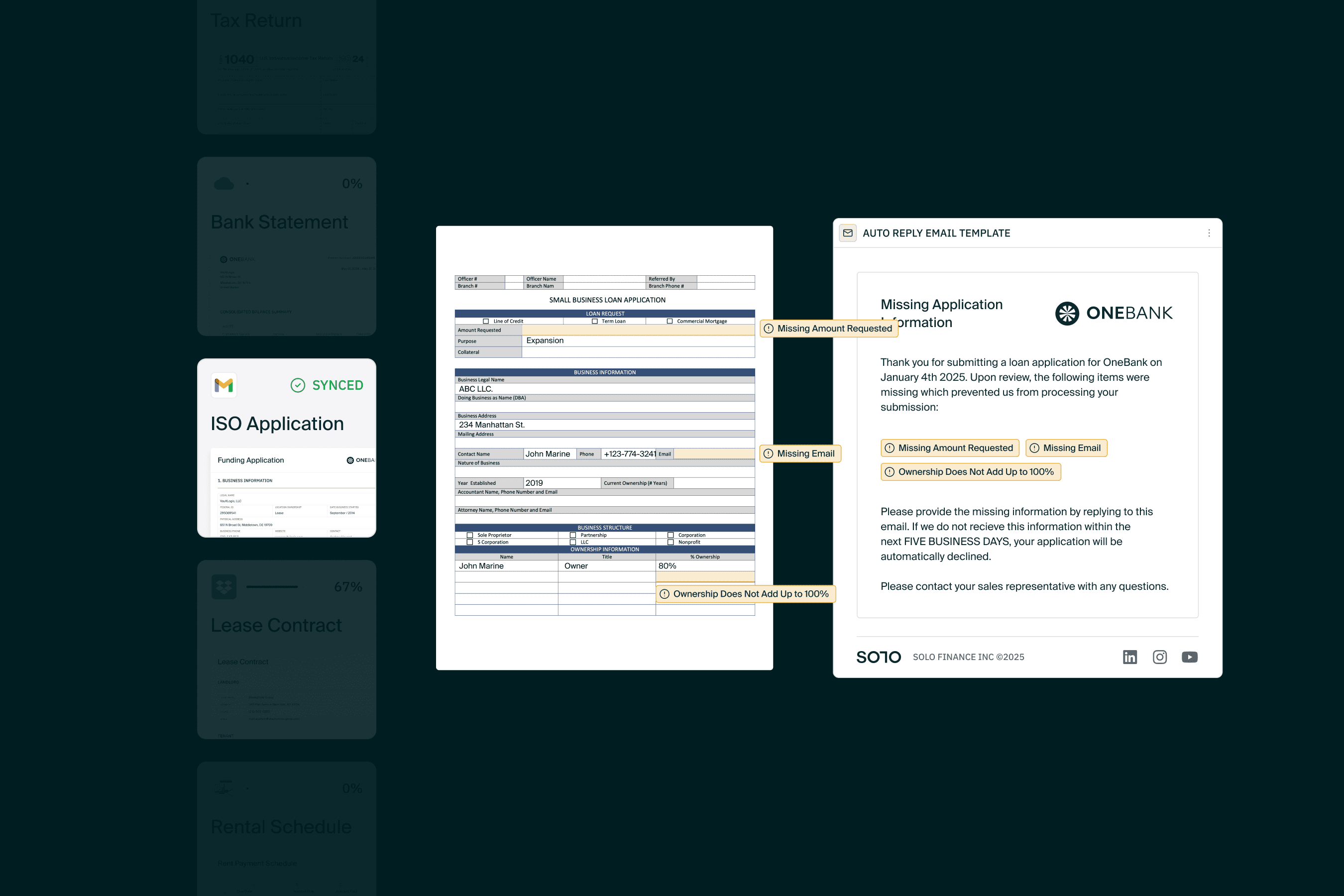

Solution: Replace self reporting with autonomous reporting to streamline data collection and interpretation, empowering underwriters with automated processes they can trust.

Autonomous Reporting: the use of automation to collect, verify, and rebuilt from raw data into financial statements calculated to the exact standardizations of the deciding entity.

In this process, a customer’s financials should be:

Deconstructed to as many raw data points as possible, to be…

Verified first as a primary traceable source before being…

Standardized into a shared language of algorithmically calculable signals, to be…

Reconstructed into a new record of truth that reveals real meaning, trusted at every level.

The insights mined, in turn, are the bedrock powering informed decision-making. We refer to this as a shift from self reporting to autonomous reporting.

Roadmap for Scaling Underwriting Processes with Digital Lending Software

Start with raw information sources: Identify and collect all relevant documents and data points needed for underwriting.

Customize the reporting engine: Set up calculations within SOLO to process raw data according to the bank’s standards.

Establish file types: Map file types currently used in the process for seamless uploads and integration into the reporting engine.

Replace self-reporting with autonomous reporting: Transition from manual data input to automated data collection, document creation, and verification.

Integrate accounts in external data sources: Connect a loan application with integrations for applicants to provide traceable, accurate raw data on demand.

Develop automated decisioning rules: Create and refine algorithms by product and context for complex underwriting processes.

Continuous optimization: Regularly review and improve the process with full visibility into data usage, customer financials, and credit potential in context.

Priority: Streamline Verified Data Collection

Solution: Create applications that leverage data integrations to collect consumer permissioned data, straight from the source and verified on demand, updated in real time.

In our 2024 State of Credit Report, the majority of C-Suite Bankers surveyed shared a similar sentiment:

“When we’re talking about paper back and forth, it’s a nightmare.”

“If people aren’t staying on top of their responsibilities for data collection, it’s taking time away that they need to be spending on other responsibilities. I become concerned about the level of time that servicing takes our team.”

Another shared that their bank endures a major reputational risk and an inability to stay competitive when they’re not able to turn product requests around quickly. For those with these concerns top of mind, it would be best to prioritize a digital lending system that can function as a single source of truth for credit teams.

Roadmap for Streamlining Verified Data Collection with Digital Lending Software

Select integration partners: Choose data providers to include based on your financial institutions’s current usage and underwriting policies.

Implement API connections: Establish secure API connections within a loan application.

Customize the application: Create intuitive application forms specific to your bank process.

Create data standardization protocols: Develop methods to normalize data from various sources into a consistent format.

Implement real-time updates: Set up systems to refresh and update customer data automatically at regular intervals.

Trace data to the source: SOLO’s system allows lenders to trace back financial calculations to their most basic forms of data, offering enhanced visibility for risk and credit teams into final calculations.

3.) Priority: Improve Low Conversion Rates on Loan Applications

Solution: Optimize applications with seamless document collection, verification, and decisioning.

Roadmap for Improving Low Conversion Rates:

Properly incentivize a completed application:.

Simplify the application process with data integrations: Streamline the information input burden on borrowers by integrating accounts for users to permission access to their financials.

Use pre-fill options: Leverage integrations to pre-fill application fields where possible, reducing user effort.

Optimize for mobile: Ensure the application process is fully responsive and easy to complete on mobile devices.

Conduct A/B testing: Continually test different versions of the application to identify which elements lead to higher conversion rates.

Analyze key drop-off points: Identify where in the application process users are suspected to abandon their applications.

Once an application is created, continue to monitor and improve. When experiencing low conversion rates, digital teams should first identify any prominent patterns in the user behavior to:

Re-assess user journey frame.

Is your prospect just researching, or actually ready to apply?

Are they ‘Sales’ ready? If not, what information or incentive do they need to become Sales ready?

Re-assess your value props.

Are you incentivizing correctly?

Are you communicating those incentives correctly?

Re-vise your approach.

Are there other sources that can replace those causing drop offs?

How necessary is this source for credit?

How should the risk-incentive model account for this drop off.

And finally, a key component of building applications that convert is an efficient decision for the borrower’s effort. Feeding inputs into an optimized a decisioning process that expedites the decision to as little as 24 hours is a compelling offer to incentivize more application fills with high conversion rates.

Priority: Unify Systems in Siloes After Loan Approval

Solution: An end to end automated flow of information between systems, where each tool talks to the other, and information is consolidated into meaning in one single source of credit truth.

This priority is best illustrated by this excerpt from our 2024 State of Credit,

"One surveyed bankers shared that they are unsuccessfully relying on Ncino and Outlook to streamline data collection. Another said they are attempting to use Jack Henry but that “Jack Henry isn’t our best solution, but it’s a step on a path towards automating this workflow.”

One banker said they’ve put a task force together to improve their onboarding process and sew together internal engines that aren’t speaking to each other.

Finally, another banker said they try to rely on strengthening relationships with customers to improve this process.

None had a streamlined process to automate monitoring and leveraging expansion opportunities over time."

Roadmap for Connecting Siloed Systems:

Document current tech stack: Understand current capabilities and each platform’s potential function.

Identify disconnects and gaps: Decide if systems need to be replaced with a better solution, or if they can be re-optimized leveraging a connection. Note where gaps highlight no solutions in place.

Strategize a framework: Reference the OneTrust Framework for our philosophy on what a unified framework should look like.

Streamline data ingestion: Utilize account integrations to collect and verify first party data.

Feed data into a dynamic reporting engine: Leverage custom reporting with connectivity built in to keep systems speaking with each other.

Maintain connectivity to data with API integrations: Ongoing connections to data enable systems to stay synced.

5.) Priority: Profitability.

Solution: Establish a infrastructure that reduces friction at every point and turns data collection from costly asset to revenue opportunity.

The right principles applied to data collection will eliminate friction while reducing risk simultaneously, creating better margins that can be passed on to the customer and bank.

Create the Highest Conversion Application (Roadmap above): Reduce friction and drop off rates to retain the maximum return on investment from customer acquisition costs.

Scale Underwriting Bandwidth (Roadmap above): Reduce costs over time from added underwriting bandwidth without incurring additional costs.

Optimize Spreads to Cover Costs: Clear visibility into borrowers financials, performance, and margins enable strategy teams with insights for

Continuously Underwrite for Proactive Product Matching: Identify new opportunities for expansion within existing base to shrink acquisition costs by increasing individual customer lifetime value at scale.

Iterate with A/B Testing and Experimentation: Remain adaptable to maximize profitability over time, with A/B testing leveraged at every part of the process to optimize key friction points.

The Go Forward Plan: Iterating on a Digital Lending Platform

Launching a digital lending platform is an iterative process. It is crucial that lenders enlist a tech stack that allows for continuous refinement and optimization throughout the end to end flow of the digital lending platform.

Having a flexible, low code system that allows for easy modifications and A/B testing is crucial for lending teams focused on maximizing profitability. This type of platform enables teams to:

Make quick changes without rebuilding the entire system each time

Adapt to changing market conditions and customer needs

Implement learnings from each iteration efficiently

Launching a Minimum Viable Product (MVP) and Maximizing Revenue with A/B Testing

Once a Roadmap is decided, banks should build a Minimum Viable Product (MVP) for digital lending that can be deployed efficiently to begin collecting baseline data for future tests.

Although processes may differ, the standard MVP we observed most often fit the following product profile:

An Application Powered by Account Integrations

Data Collection Feeds Into Lender-Built Reporting Logic

Autonomous Reporting Powered by Raw Account Data

Continuous 360 Degree Underwriting

Once an initial digital lending platform is launched, SOLo recommends A/B test applications, reporting, and lifecycle management to reveal opportunities for optimization and growth.

Key Metrics to Track In A New Digital Lending Platform

A quick snapshot of primary metrics for tracking digital lender platform performance.

Metrics Indicating Overall Platform Performance and Profitability:

Time to Decision

Application Conversion Rates

Funded Application Volume

Customer satisfaction scores

Loan performance indicators

Metrics Indicating Application Performance:

Conversion Rate: % of Traffic Turned Into Opportunities

Time to Complete

Application Drop Off Rates by Page or Field

Account Integration Opt In Rate by Source

Metrics Indicating Underwriting Model Performance

Cost To Underwrite (by Application)

Approval Rate

Number of Applications Processed

Time to Decision

Ease of Use

SOLO’s credit data infrastructure was developed to support the processes of lenders and their ability to adapt platforms for future resilience as they launch digital lending platforms. We built SOLO as a streamlined, low-code solution to enables continuous expansion and optimization, comprised of a robust data ingestion platform, reporting and spreading engine, and portfolio management tools enabling banks with solutions for today and power for shaping their futures in digital lending.

Explore additional Resources to further support lenders in their digital transformation journey, including expert consultations with industry leaders, digital lending toolkits, and product demos customized for your process.

About SOLO

SOLO’s data ingestion platform transforms how customer financials are collected and activated for banks and lenders. Backed by a network of 100+ community banks, SOLO developed a product for and alongside bankers to drive 40% underwriting cost reduction while improving LTV per customer. The digital lending technology features frictionless applications, continuous 360 underwriting, and proactive product matching. Lenders gain instant and constant visibility into a customer’s eligibility for services in house or in their preferred partner network, all from a single seamless application.